The Protein Revolution - Part 1

Every one of us consumes food, but not many of us understand the impact of our food beyond filling our stomachs.

“100 million people are starving. 1.3 billion tons of food is wasted every year. We do not need to produce more. Instead, we need to act differently.” Chef Massimo Bottura

Every one of us consumes food, but not many of us understand the impact of our food beyond filling our stomachs. The environmental damage caused by our food supply is unimaginable. Each year, we slaughter 330 million of cattle, 1 billion of sheep, 1.5 billion of pigs, and 66 billion chickens. To rear these animals, we need 32.1 million km2, equivalent to the size of Africa. Not only that it leads to large scale deforestation, but global animal production also requires about 2422 Gm3 of water per year. Furthermore, cattle are also the largest contributor to methane, which makes up 10% of greenhouse gas. Least to say, land and water are revoltingly wasted, and the meat we consume is speeding up climate change. While we shout “bon appetit!”, Mother Earth is struggling to feed us.

Not only that the way we consume food is terrible for the environment, but it is also highly inefficient. According to the United Nations, an acre of land used for raising cattle would yield a mere 20 pounds of protein, while that same acre would yield 365 pounds of protein when used to cultivate soybeans.

Philanthropists, scientists, and entrepreneurs around the world have been seeking sustainable solutions to this – how can we produce food differently with less time and resources (and potentially cheaper)? Alternative protein is one of the answers they found.

What is alternative protein?

Alternative protein is a catch-all phrase that can be interpreted as proteins derived from non-animal sources. Usually referring to plants, microbial (fermentation), insects, or through tissue culture to replace conventional animal-based sources. It is important to bear in mind that alternative proteins are not just seeking to replace nutritional content through alternative sources, it aims to replicate the sensory experience (if not improve it) of consuming traditional animal proteins.

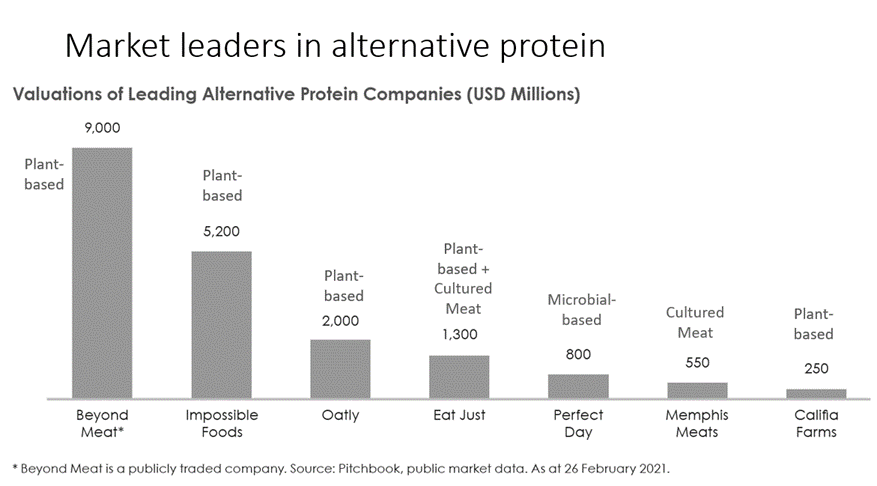

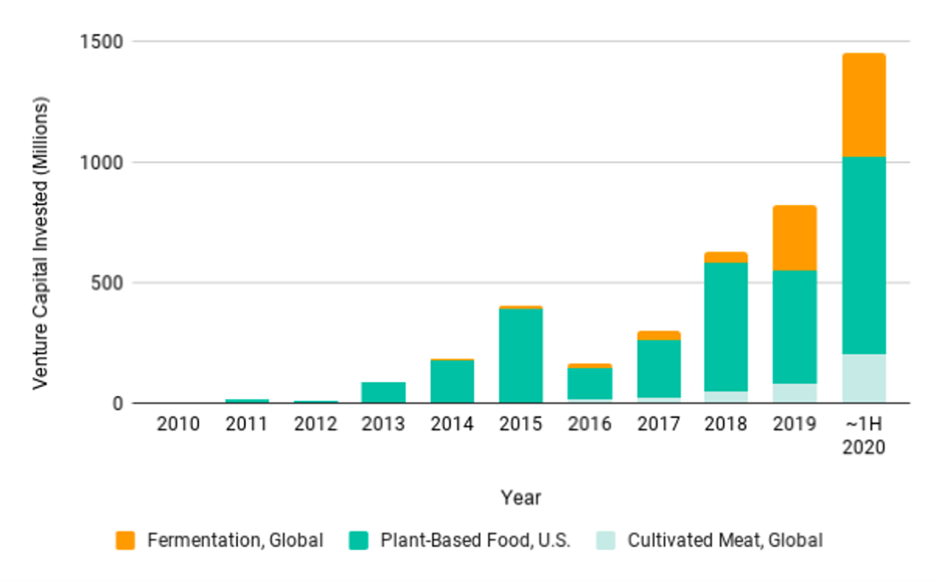

What does this mean to investors? Well, billion-dollar businesses such as Impossible Foods, Beyond Meat, Oatly, and Eat Just, have emerged in this new sector. According to the Good Food Institute, a record-setting $3.1 billion was invested in alternative proteins in 2020. However, plant-based is only the beginning. An increased amount of capital is also flowing into cultivated meat and fermentation。

The spotlight has been on California when it comes to alternative protein for a while, Israel has also been catching attention in recent years, and we continue to believe that exciting alternative protein start-ups will emerge from these regions because of their advanced technology know-hows. However, our view is that investors are underestimating the alternative protein opportunities arising from China and overlooking the unique edge it has, particularly in fermentation.

However, our view is that investors are underestimating the alternative protein opportunities arising from China and overlooking the unique edge it has, particularly in fermentation.

Plant-based Protein

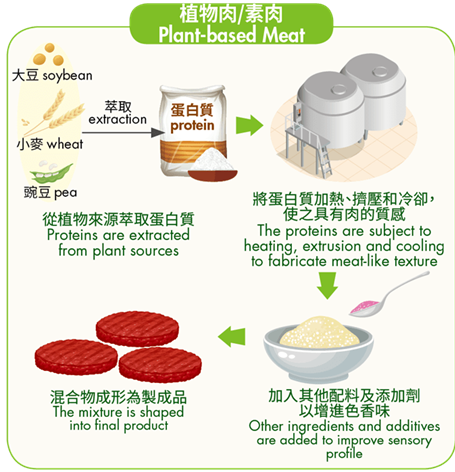

Plant-based proteins are created by extracting protein concentrates from plants, such as peas, wheat, soy, chickpea, canola, and corn. After extraction, the proteins are subjected to heating, extrusion and cooling to fabricate meat-like texture. Other ingredients and additives are added to improve sensory profile. Finally, the mixture is shaped into final product.

Speaking of plant-based protein, most will immediately think of market leaders such as Impossible Foods and Beyond Meat. The key differentiator with the two brands lies with their formulations. Impossible Foods has a patented soy leghaemoglobin protein produced using yeast fermentation which gives the Impossible Meat the bloody taste of real meat. Beyond Meat, on the other hand, uses coconut oil to replicate the marbled look of meat and beetroot juice to mimic blood and browning effect.

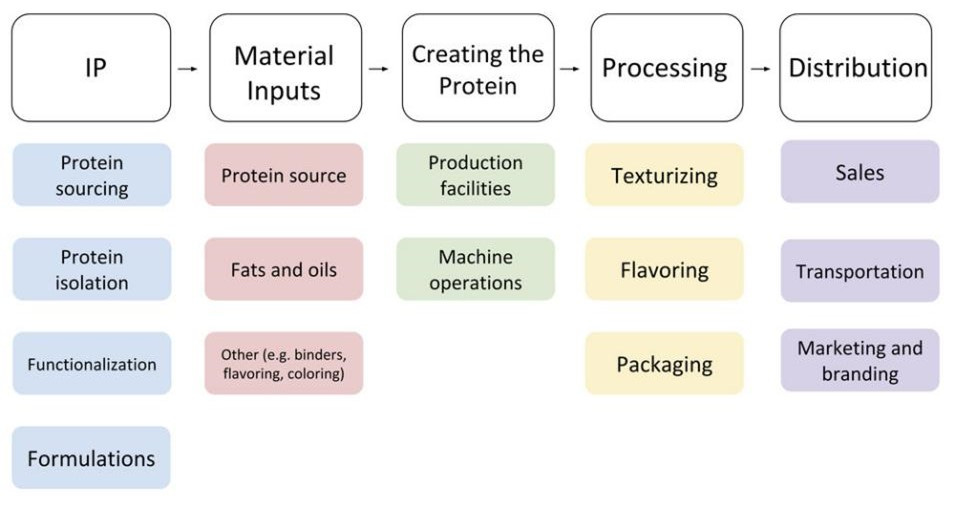

However, despite the different formulations, most plant-based protein companies use the same extrusion technology and similar protein source. This makes it difficult for plant-based protein companies to develop strong moat and is highly reliant on branding and marketing. In our view, the stars for plant-based protein are already born and it will be increasingly difficult to compete for consumers’ mind space. The investment opportunities lie in the upstream such as plant breeding, protein sourcing, and protein isolation.

Plant-Based Protein Value Chain

Cell-based Protein

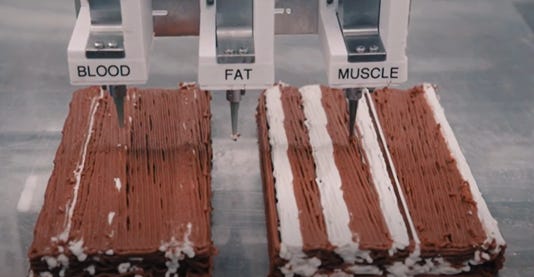

Cell-based proteins are an attempt to grow meat parts in a controlled environment, without growing the entire animal. In order to do so, stem cells are extracted from a live animal then grown in a nutrient rich culture within a bioreactor. The cells replicate, and form either muscles, fat or connective tissue. These are then used to recreate the meat of the animal from which the stem cells were originally harvested.

As of now, cultivated meat comes out like high school romance - mushy. We can grow a hamburger patty, but not something like a steak, which requires a more solid physical form. Currently, scientists are exploring ways to give cultivated meat the structure they need to resemble a cut of meat. The most commonly explored ways are (1) scaffolding, the scaffold is basically a mould of the object you want your cells to turn into. It is put inside the bioreactor for the cells to grow on (gelatin/collagen/plant fibre) so they can get organized while the cells get specialized; (2) 3D Printing, by extruding the cells layer by layer until it forms a particular shape. Israeli start-up, Redefine Meat, has built their own 3D printers specially for alternative protein printing. However, both methods are challenged by scalability. That being said, despite the search for a perfect lab-grown cut of meat, 60% of the meat consumed in the US (12% of global meat consumption) are actually in grounded form, so there is still huge market opportunity even if we don’t solve the meat structure problem any time soon.

The more urgent challenges are scalability, cost, regulations, and psychology hurdle.

Uncertainty Around Cell Lines: Access to cell lines from species used for cultivated meat production is the major barrier for new research endeavors. There are a lot of questions around which cells will be best suited for large-scale manufacturing or the creation of specific product types. Except for chicken (chicken embryo is actually widely used for vaccine research), a lot of cells are not well-researched for cultivated meat.

Mass Production Difficulties: There are simply not enough bioreactors in the world, meeting just 10% of global meat demand will require over a million bioreactors. Thus, companies are trying to improve bioprocess design and develop industrial scale bioreactors. High degree of control is needed for optimal production of cells, i.e. regulation of PH levels, temperature, oxygen and carbon dioxide levels, etc, and all these are yet to be experimented in an industrial production set up.

Sky High Cost: Basal media (glucose, amino acids, vitamins) together with growth factors (recombinants of FBS) represent 60-90% of the cost of cultivated meat. Historically, cellular agriculture companies have used pharmaceutical-grade growth media, which is inherently very expensive ($400/liter) given the high precision and need for providers to comply with extensive regulation. Food-grade media is being developed and there is research around media recycling, however, and the price of growth media is declining rapidly, bringing down the cost of cultivated meat at a dramatic pace from $325,000 for a regular beef patty in 2013 to $11 per patty or around $7 per pound in 2019. Despite the very positive trend, cultivated meat still need to significantly decrease its price in order to compete with traditional meat products which costs just $2.80 per pound.

Regulations and Consumer Perceptions: As of today, the only cultivated meat product that has been approved for commercial sale in the world is GOOD Meat by Eat Just, which was approved by regulators in Singapore in Dec 2020. Even though it is expected that US and Europe will catch up on the approval of cultivated meat products, it will still take some time for consumers to accept the idea of cultivated meat.

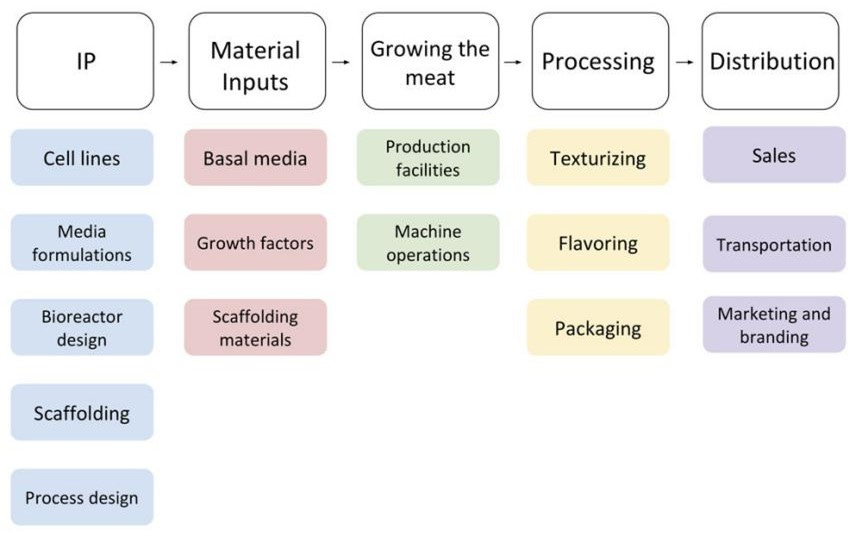

Cultivated Meat Value Chain

Challenges always come with opportunities. Companies who can solve the pain points of high cost, scalability and texturizing are set to win the cultivated meat race.

We will continue the discussion on fermentation in Part 2 of this article.

The Present Value of the Future is a series of thought pieces written by Star Magnolia Capital’s analysts based on our long-term thematic research projects. Although our company-level investment activities are executed by our external managers, we believe we become better and patient investors by conducting our own thematic research. In this way, we can stay relevant and build our own knowledge base. Our thematic research is often inspired by insights shared by our external managers and then produced with publicly available or proprietary sourced information. We share our own research because communication is an often-underappreciated tool to gain trust. We want to help our readers understand the dynamic changes and opportunities we see in the world today.

Past Publications

| A guest post by

|