You Can Copy Ideas, but Not Convictions

Why Don’t We Copy Ideas?

Star Magnolia Capital advises families to manage their portfolios of great investors. Many investors focusing on public markets manage their portfolios of highly concentrated, long-term investment ideas. Quite often, their portfolios include only 10-20 names and hold the same names for 5-10 years. Sometimes they own the same companies over 20 years (see this investoon about Arisaig’s 20+ year investment in Vitasoy as an example of the returns that such a long holding can bring). Some families ask us why we focus on advising on investing in managers, rather than investing directly into the portfolio of stocks. We could look at public disclosure (such as SEC Form 13F) or monthly letters from investment managers and copy these names.

The Apple Trades

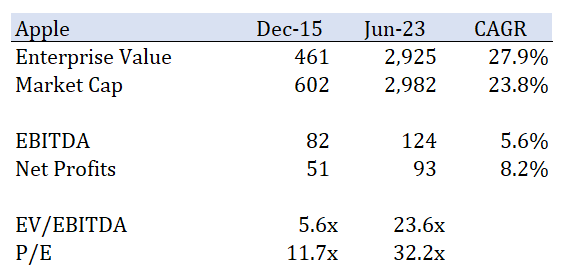

In theory, it is possible, but we do not think that we could generate the same type of returns as our investment managers if we simply copy their portfolios. For example, it does not require a Ph.D. to copy Buffett’s public holdings, but most people can rarely match his return. In 2016, Buffett’s Berkshire Hathaway famously acquired 9.8 mm shares of Apple at around $22-24 for $210-240 mm. They kept buying Apple shares over the last 7 years and have accumulated 916.6 mm shares, which are valued today at $174 bn (23% of Berkshire Hathaway’s market cap). The return on the first purchase (without dividends) was 825% (35% p.a.).

Berkshire Hathaway made so much money on Apple not because they knew something others didn’t know, but because they saw something others didn’t care to see. At the end of 2015, Apple’s market cap was $602 bn and trading at 11.7x P/E. The valuation multiple was even more attractive in EV/EBITDA as Apple at that time had a lot of cash on the balance sheet and no debt. Today, Apple’s market cap is close to $3 trillion and trading at 32.2x P/E and 23.6x EV/EBITDA. The share price appreciated because Apple continues generating healthy profits at 8.2% CAGR… wait, only 8.2% CAGR?

In fact, what Berkshire Hathaway saw in Apple 6 years ago was not the iPhone maker’s spectacular growth, but its cheap valuation. They didn’t need to make a bet on the unforeseeable future of how many iPhones will be sold. They only needed to know that people will continue to use the iPhone.

The Carry Trades

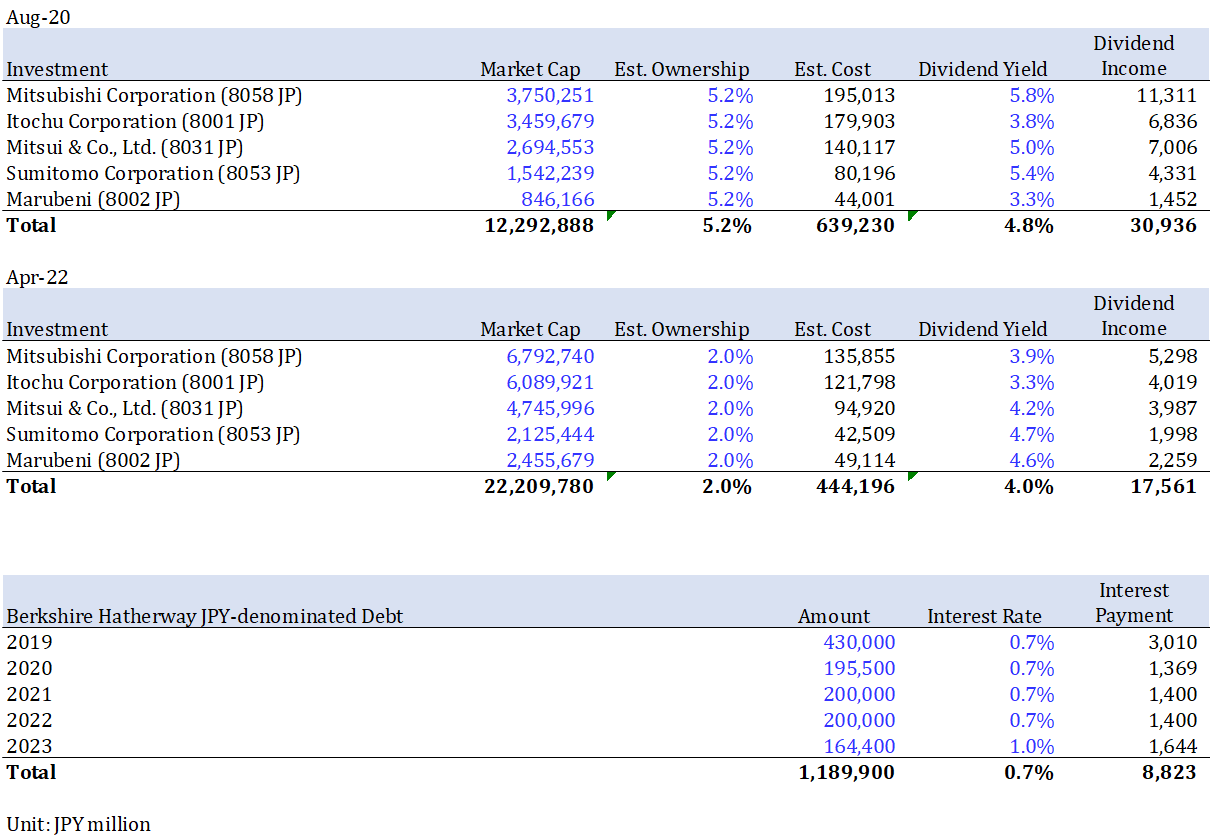

In 2020, Berkshire Hathaway also acquired shares in 5 trading companies in Japan for approximately JPY 640 bn ($5.9 bn). Some people paid attention to this trade, but most didn’t and forgot about it. It was in 2023 when a lot of people started paying attention after Berkshire Hathaway made so much money (and also added a little bit more positions).

I’m amongst the many investors who dismissed Buffett’s investments in Japan, partly because I’m always too negative on Japan, but partly because I didn’t quite understand why he was very interested in those companies.

Many people believe that Buffett is very bullish on Japan as Corporate Japan finally woke up. And, quite conveniently, the valuation seems to be still attractive. However, if you know the business nature of the trading companies well, and how these trades are structured, you will know that Buffett is not necessarily bullish on Japan. It’s actually quite the contrary.

In Aug 2020, the five trading companies (Mitsubishi, Itochu, Mitsui, Sumitomo, and Marubeni) were trading at very cheap valuation (5-7x P/E), but the low valuation was found everywhere at that time due to the global pandemic. What Buffett saw and others didn’t was a great “carry trade” opportunity. Thanks to Japan’s three-decade-long zero interest rate policy, despite the pandemic, Berkshire Hathaway was still able to issue JPY-denominated debt at 0.7% and he was able to finance all the acquisitions with very little equity at risk. At the same time, those Japanese trading companies were paying an average of 4.8% dividends. Thus, Berkshire was able to enjoy the spread at 4.1%, with very little equity exposure. Of course, the trade was not risk-free as they still had to cover the losses on the trading companies if the share prices fall, but a substantial part of the downside risk was mitigated by the health spread of the dividend Berkshire received (4.8%) and the interest Berkshire paid (0.7%). What made the trade even more attractive is its natural currency hedge against JPY. Obviously, they had very limited JPY exposure as they acquired stocks with the proceeds from JPY-denominated debt. At the same time, the trading companies are usually beneficiaries of weak JPY as they operate and own assets outside of Japan (for Japanese companies). In fact, JPY fell from 108 (USD/JPY) to 138 (USD/JPY) in three years (down 21%). Without the JPY hedge, Berkshire’s return on the trading companies could be 21% lower.

The estimated return on these five trading companies, including dividends, is 127% in JPY and 85% in USD. If Berkshire Hathaway bought Nikkei 225, instead of the trading companies, its JPY return would be 48%, but its USD return would be just 21%. So, he definitely didn’t buy “Japan”. In fact, the exposure to Japan’s domestic economy through trading companies is quite limited.

It could be very challenging to copy Buffett’s trade in 2020 because the world’s future was so uncertain. Buffett was able to buy because he was able to build the trades with several natural hedges. He was also able to finance the entire trade without investing a lot of equity. After all, he didn’t take a lot of risks that he couldn’t control. He had high conviction in the trade, not in the companies, and without Berkshire Hathaway’s balance sheet, you would not be able to construct this “carry trades” (note: a carry trade is a trading strategy that involves borrowing at a lower interest rate and buying an asset that provides a higher return. It helps investors to enhance returns as investors can build large positions with borrowed money) with very little equity at risk. This low-risk profile of the trade, I believe, was translated into Buffett’s conviction.

We Cannot Copy Convictions

One of our investment managers recently told us that they are not worried about the risk of their highly concentrated, long-term portfolio being copied. Whoever has access to their portfolio data can copy and it is not very difficult in this digital era, but they don’t think others can achieve the same returns because the copycats cannot copy the investment manager’s conviction, which is based on lengthy in-depth research as well as structural advantages. In the case of Buffett’s Japan Trades, it was Berkshire Hathaway’s balance sheet. For others, it could be the relationships they have built with the company management, pattern recognitions of businesses in various industries over multiple cycles, or unique knowledge and expertise in certain markets, to name a few. Because investment managers build deep convictions in these investment opportunities, they are better able to maintain high concentration in certain portfolio holdings during challenging times, or even take advantage of market drawdowns and double down on these holdings. At a more fundamental level, emulators lack the insight that forms the bedrock of an investment manager’s deep conviction in an investment idea in the first place. Copying the ideas of a brilliant investor might therefore be akin to building a nice house on loose sand, and we should never forget that behind every deep conviction is an investment insight - and that this insight is a product of a manager’s compounded knowledge (in a particular industry, type of trade, etc) that should be respected for its complexity and its role in driving superior returns. That is why we seek experts and entrust our capital with them.

Read previous posts:

We Are Experts of Nothing, But Finding Experts

Two Professors Prof. Lauren Cohen is a leading scholar and educator at Harvard Business School. We were introduced to Prof. Cohen by Prof. Tony Gao at Tsinghua University PBC School of Finance (Tsinghua PBCSF), who is undoubtedly the most prominent academic researcher for family office research in China. In 2012, Prof. Gao was appointed as Director of th…

Star Magnolia Capital in Search of Hua Mulan

Her Name is HUA Mulan: Star Magnolia Capital was named after a white-flowering tree originating from the highlands of the Japanese island of Honshu where her founder was born. Her seeds were planted in Hong Kong and bloomed in Shanghai and Singapore. However, there is another star magnolia that inspired us. Her name is HUA Mulan.

Preserving Legacy for Families

Brandywine Creek Brandywine Trust Group, LLC, a multifamily office, which manages over $10 bn, is located within a few minutes from Brandywine Creek, where General George Washington lost a critical battle against the British Army. This defeat resulted in the fall of Philadelphia, then the American capital. Today’s Brandywine Creek is picturesque na…

Investing in companies and investing in managers sometime are the same as both decisions are capital allocation; Just think about investing in BRK, is it investing in companies or investing in manager? Should be the same if it is within a coherent framework