Japan in the Garden of Good and Evil

Sawada, the Sushi Chef

Sawada is a tiny sushi restaurant with only six seats in Ginza, Tokyo. The experience begins as your hand slides back the wooden door; your heart beating with expectation. Immediately, Chef Sawada greets you from behind the counter. He carefully molds each piece of sushi according to each customer based on his long experience: Hungrier customers want large rice, drinking customers want to start slowly. Thus, Chef Sawada hates customer’s late arrival because he times the rice so that it will be at perfect temperature for each customer. Sawada is a role model for Star Magnolia Capital – this is how we serve our clients. Best performance and quality – only for you.

Going Gung-ho

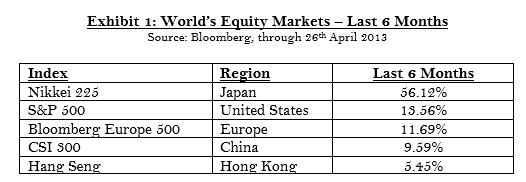

Since I wrote my last letter, In the Mood for Speculation, in October 2012, the Japanese stock markets performed really well, not only generating the best return among the major stock indices (See Exhibit 1), but also the best 6-month rolling return since the Bubble Economy period, 1986-1991. The new prime minister’s economic policy and the Bank of Japan’s Quantitative-and-Qualitative Easing Program successfully have converted depression paranoiacs into optimists. I was too bearish to prepare for the rally.

However, I’m also seeing a sign of exuberance in the Japanese stock market. Gung-ho Online Entertainment is a public Japanese video game company and is a poster child of Japan’s recent stock market rally. Over the last 12 months, this company’s share price shot up by 4716% (Exhibit 2) and its market capitalization increased from USD200 million to over USD10 billion, ranking it among 100 largest companies in Japan. The firm’s best known games are Ragnarok Online and Puzzle & Dragons, and 12 million copies of Puzzle & Dragons were already downloaded in the first 16 months (e.g., Angry Bird, the most popular mobile game, reached a billion downloads early 2012). Gung-ho’s valuation of 23 times of the next year’s earnings is based on 400% growth of revenue and earnings and looks frothy to me.

Fallen or Still Falling?

Asked about my view on the Japanese yen in the last few years when the currency was trading between 75 and 80 per the US dollars, I said my target price was 200, or 60% drop. I felt I was a boy crying wolf. When the wolf actually showed up in the village, those bullish analysts quickly became very bearish and told their clients “I told you so”. That is how the financial industry works.

From a real economic point of view, the Japanese yen was not so expensive as everybody believed. The real effective exchange rate of Japanese yen has been falling for the last two decade, making the relative price of Japanese products cheaper (See Exhibit 3). Many Japanese manufacturers complained about the expensive Japanese yen, pointing at the JPY/USD exchange rate, but they all forgot that the United States also pushed her own currency lower to boost exports, and China became increasingly more important trading partner for both imports and exports. Over the last 10 years, the Chinese RMB has appreciated 11.5% while Japan’s domestic price fell 13% (based on GDP deflators). The two decade long economic slump in Japan is not due to the strong currency, but domestic and structural issues such as persistent deflation, rapid ageing and sluggish domestic demand.

Kuroda’s Box

Haruhiko Kuroda, newly appointed chief of the Bank of Japan, is not a typical Japanese – he is vocal, confident and decisive. At the first policy meeting, Kuroda announced that the Bank of Japan would aggressively inject liquidity into the economic system and achieve a 2% inflation goal within the next two years.

In the Greek mythology, Zeus gave the curious Pandora a large locked jar and to Epimetheus its key, saying it should never be opened. During Epimetheus’s absence, Pandra stole the key and opened the jar, releasing all the evils of the world. Remained, however, in the jar was Elpis, the Spirit of Hope. Milton Friedman, the father of monetarism, gave Kuroda a box, which he was too curious not to open. He released liquidity in the system and was celebrated with the strong stock market rally.

In the economics term, the hope that remained in Kuroda’s box is called inflation expectations. Since inflation is both a monetary and a psychological phenomenon, Kuroda’s mission is to change how Japanese think about inflation. For central bankers, management of inflation expectations has been a very important policy tool, but its primary goal was to keep inflation low. Contrarily, Kuroda is probably the first central banker to use it to keep inflation high.

The initial euphoric mood will soon dissipate once corporations and investors realize that Kuroda’s new monetary policy will weaken the Japanese yen beyond the economically fair level - about JPY 100-120 per USD; and then, they will start to move their capital overseas. The rates of return on investment overseas for Japanese have already been far higher than domestic businesses (See Exhibit 4) and outward investment has also been a secular trend over the last decade (See Exhibit 5). Softbank’s $20 billion offer for Sprint indicates an increase in similar cross-border transactions by Japanese investors.

During the interview with CNBC on 5th April, George Soros explained what would happen to the Japanese yen market once a consensus is formed.

“So if what they are doing gets something started, they may not be able to stop it. If the yen starts to fall, which it has done, and people in Japan realize that it is liable to continue, and want to put their money abroad, then the fall may become like an avalanche.”

Weaker Japanese yen will further encourage Japanese companies to move their capital away from Japan, and this action will further weaken the Japanese yen. As the Japanese yen loses its buying power, prices of imported goods will increase and people will expect inflation to start rising. In this scenario, Kuroda will achieve the 2% inflation goal without reinvigorating the economy – a conundrum the Bank of Japan hasn’t faced for twenty years. Nietzsche said hope may be the worst of all evils because it prolongs the torments. The Japanese economy has a right to hope for a better growth and higher inflation, but this hope can be very harmful.

Who is Stuck with the Old Maid?

The 20-year effort to escape from deflation left Japanese with a huge pile of the government debt, which will become approximately 240% of GDP by 2014. The Japanese government is paying more than 50% of the tax revenue to pay the interests and rollover maturing debt. This situation is clearly not sustainable.

The Bank of Japan’s attempt to generate higher inflation should help the government to manage the debt pile, but investors of the Japanese government bonds (JGBs) will suffer substantial losses as the bonds lose their value as the inflation increases. We haven’t seen any sell off in the JGB markets, but this $15 trillion market is also changing quite dramatically.

There are three major investor groups in the JGB market: Private Financial Institutions (banks and insurance companies), Semi-Public Entities (Japan Post and pension funds) and the Bank of Japan. All combined, three groups own more than 80% of the outstanding. From 2000, the Japan Post became a major player in the JGB market and the Semi-Public Entities increased their market shares by 20% in less than ten years. However, after the privatization of the Japan Post in 2007, the Private Financial Institutions aggressively increased their holding in JGBs and regained the top rank in 2011 (See Exhibit 6).

After the banking crisis in 1997, which resulted in broad consolidation of the industry and nationalization of a few major banks, Japanese bankers became risk averse and reluctant to originate new loans. They would rather make almost zero returns on JGBs than being criticized. Over the next 15 years, Japanese banks reduced their loan portfolio by 15% and almost simultaneously increased JGB holdings (See Exhibit 7) in proportion.

In 2012, this trend changed, and the reason was obvious. According to the report issued by the Bank of Japan in October 2012, Japanese banks would face a total of JPY 6.7 trillion in losses should interest rates broadly rise by 1%. This means that if Bank of Japan successfully increases inflation from current level (-0.9%) to the target (2.0%) and the yield curve is shifted upward by the same amount, Japanese banks will face JPY 20 trillion in losses, or 40-60% of banks’ Tier 1 capital. The best way to avoid the losses is to sell their massive investments in JGBs.

Over the same time period, Japanese insurance companies also became a dominant buyer of long duration JGBs as they needed to narrow the duration gap between their assets (bonds and equities) and liabilities (future payouts). As a result, the insurance companies’ shares in the super-long-term JGB market rose from below 30% in 2004 to almost 45% in 2011. However, this trend is also reversing because of acceleration of ageing and anticipation for higher inflation and nominal interest rate.

While both Private Financial Institutions and Semi-Public Entities are reducing their exposure, the Bank of Japan is increasing its JGB holdings aggressively. According to Goldman Sachs’ estimate, the Bank of Japan will purchase more than JPY 130 trillion worth of JGBs through the end of 2014, raising its share from 12% to 23% (See Exhibit 8). In another word, Bank of Japan will eventually absorb almost 50% of new issuance of JGBs when other investors are selling.

Sooner or later, the Bank of Japan will realize that all other players have left the play room and the central bank is stuck with the old maid. The Bank of Japan has no option but continues buying JGBs not to let rising interest rate destroy the economic recovery. However, this is the same path many deeply-indebted governments got into serious trouble and ended up with hyperinflation.

Kimura, the Farmer

Akinori Kimura, a Japanese farmer, grows apples. Years ago he came across Masanobu Fukuoka’s book, One Straw Revolution, which inspired him to cultivate his own apple trees without use of pesticides or fertilizers. He had a very hard time converting his orchards because apples are very vulnerable to pests and diseases. However, after years of tremendous effort, he finally succeeded. Until I read this book, I have never thought how difficult it could be to grow organic apples.

If you visit an apple orchard during summer, apples are often covered in white with pesticides as farmers typically sprinkle every 10-15 days (See Apple Covered by Pesticide, next page). According to a study of the U.S. Department of Agriculture, on average, apples are the most contaminated produce, with 48 different pesticides showing up on 98% of the more than 700 apple samples tested. Even at organic orchards in the United States, antibiotics, streptomycin, and oxyteracycline are used to cultivate apples. Those chemicals are listed as synthetic materials approved for use in organic apple production, but this antibiotic exemption is set to expire in October 2014.

Kimura’s apples are now called Miracle Apples and, when they are in season, are sold out within 10 minutes on his website. And yet, he only charges each of his precious apples $3. It was not the money, but a farmer’s professionalism to produce the best apples, which led him to success.

(Akinori Kimura’s MIRACLE APPLES was translated into English by Yoko Ono and can be found via this link: http://imaginepeace.com/miracleapples/)

Conclusion

Like Satan’s temptation led Adam and Eve to gain the knowledge of good and evil, the fall of the Japanese yen will reveal both the goodness and badness of Japan. The Japanese government will be forced to make very some difficult decisions soon. However, the fall of the Japanese yen also creates some very attractive investment opportunities. For example, Japan’s high-quality services and food safety should have greater appeal to the growing population in China. We just need to be patient and wait for the moment. Sawada and Kimura are the guiding lights for the future of Japan: the culture of professionalism still exists in that small island country where I was born.