Drink Moutai, And Be Merry

Many Western investors publicly say they don’t buy Chinese stocks because they don’t understand the culture. A good example is Chinese people’s adoration for this 400-year-old brand of liquor, Moutai white liquor. Westerners describe the flavor of Moutai as “taste like barf” and I don’t categorically deny this claim. However, this stinky 53% (106-proof level) white liquor has a very strong acquired taste for Chinese people (and myself), and is now recognized as China’s national liquor. Despite its high retail price tag ($200-300 a bottle), the company produces 100,000 tons or 200 million 500ml bottles of Moutai every year.

Kweichow Moutai Co. is the sole producer of Moutai white liquor and is based in a remote town called Moutai Town in Guizhou Province. The nearest airport is located in Guiyang and is only accessible with a 3-hour car drive or 6-hour bus ride on a bumpy mountain road. Not many investors visit the company’s headquarters because of the distance. Moutai is still owned by the local government and is one of the largest taxpayers in the province.

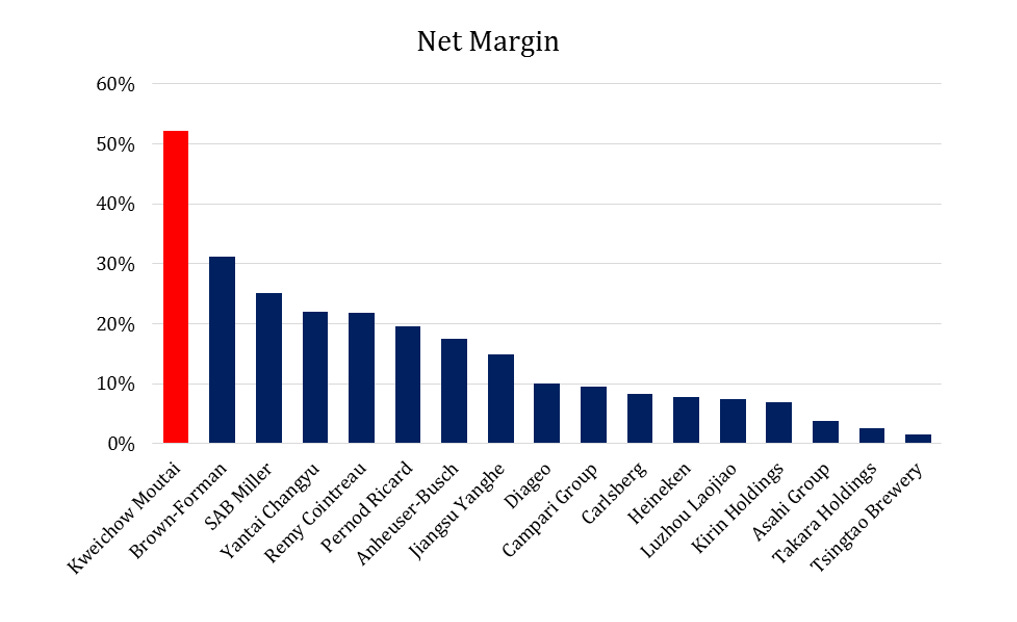

What distinguishes Kweichow Moutai from other liquor companies is not its flavor, but its quality of business, especially compared to other hard liquor companies in the world. The company’s gross margin (92.1%) and net margin (52.2%) are by far the highest among its global peers. China’s white liquor is distilled from fermented sorghum and its cost is very low. With Moutai’s premium price, the company can enjoy extremely high profitability.

Investors were worried about the adverse effects of (1) China’s slowing economy and (2) the anti-corruption campaign. Their concerns are quite understandable as Moutai’s retail price fell almost 50% from the peak level of 2012. However, Moutai’s earnings were strangely never affected by the retail price. How is it possible for a company to maintain its high margin while its only product has a sharp price correction? Is Moutai another Chinese fraud?

The investors were fooled by the two pricing structures of Moutai – the retail price and a so-called ex-factory price. Most people only see the price of Moutai at retail liquor stores and mistakenly think this is the same price Moutai is selling its products to the retail liquor stores. In fact, Moutai’s ex-factory price has risen by almost 200% since 2001, however, its price increase was much slower than the retail price. In 2012, the retail price was almost 100% higher than the ex-factory price. Since Moutai never raised or reduced the ex-factory price for the last 3-4 years, the company’s earnings were not impacted by the big swing of the retail price.

However, the biggest mystery is Kweichow Moutai’s valuation. The company’s US$ 38 billion valuation means that the share is now trading at 15x of this year’s earnings or 13x of next year’s. While the company’s valuation looks fair to its Chinese peers (15x next year’s P/E), it is significantly undervalued to its global peers. In our view, Moutai offers a very attractive long-term upside with a limited downside.

Why does this kind of opportunity exist in China? This is because there are a very limited number of institutional investors with a long-term mindset in today’s China. 99.99% of Chinese market participants are speculators in our view. We discussed our views on China’s domestic stock markets (A-shares) in our China 101010 newsletter on January 6, 2014. Since then, China’s stock markets went up as much as 150% and fell as much as 40% (still up more than 50%). And, interestingly, the valuation of our China 101010 portfolio increased marginally thanks to the strong underlying growth of those companies. Honestly speaking, to make money in China, you do not need to be extremely smart; you just need to be a long-term patient investor and invest in the companies who are beneficiaries of China’s growing middle-class consumers.