Unconventional Asset Allocation: Absolute Return

In Oct 1989, Yale became the first institutional investor to define absolute return strategies as an asset class, beginning with an allocation of 4.5%. It was one of the most unconventional investment decisions David Swensen made over the last 4 decades of his tenure. When Yale started allocating capital to Absolute Return, or hedge funds, they were not a common investment solution for institutional investors. Although hedge fund titans we know well today such as George Soros (started Quantum Fund in 1970), Michael Steinhardt (started Steinhardt Partners in 1967), Bruce Kovner (started Caxton Associates in 1983), and Julian Robertson (started Tiger Management in 1980) and started their hedge funds in 1980s, they primarily relied on high net worth individuals as sources of funding. According to Hedge Fund Research’s (HFR) data, 80% of the capital was coming from the wealthy individual investors. The Endowment & Foundations was only 2-3%.

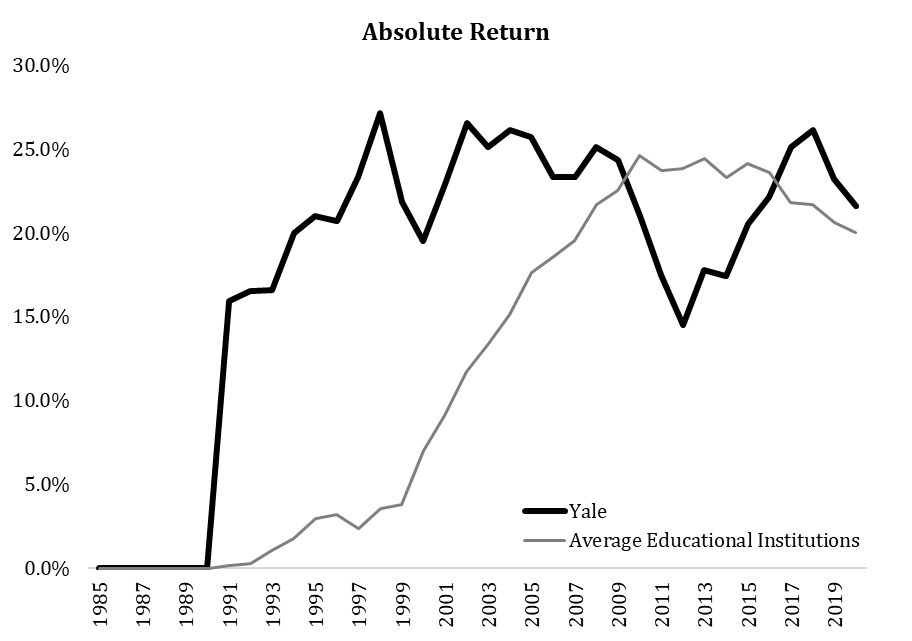

Yale allocated 15.9% of its portfolio to Absolute Return, valued at $400 mm. Again, according to HFR, the total assets under management of the hedge fund industry back in 1991 was $58 bn. That means the Endowment and Foundations collectively allocated $1.16-1.74 bn. Yale was almost 1/3-1/4 of this.

The allocation decision was even more unconventional if you know that the oldest hedge fund benchmark only goes back to 1988. The most widely used hedge fund index, HFRI, only started in Jan 1990. Can you imagine how you can propose your board of trustees or investment committee to make an allocation to the asset class which has only 2-3 years of previous benchmark data? Most people didn’t even consider it as an asset class.

In David Swensen’s own words, he describe Absolute Return as following:

“Absolute return investing, first identified as a distinct asset class by Yale University in 1990, relies on active management for its very existence. Dedicated to exploiting inefficiencies in pricing marketable securities, absolute return managers attempt to produce equity-like returns uncorrelated to traditional marketable securities through investments in event-driven and value-driven strategies. Event-driven strategies, including merger arbitrage and distressed security investing, depend on the completion of a corporate finance transaction such as a merger or corporate restructuring. Value-driven strategies employ offsetting long and short positions to eliminate market exposure, relying on market recognition of mispricings to generate returns. Generally, absolute return investments involve transactions with relatively short time horizons, ranging from several months to a year or two.” (Pioneering Portfolio Management)

In the recent interview of Ted Seides (Unlocking Investment Wisdom; he is interviewed by Sarah Samuels, the head of manager research at NEPC), he recalled the early days of working closely with David Swensen. He joined Yale in 1992, just seven years after Swensen took the office.

“It was easy to win because nobody else was doing what David was doing.”

One of the examples was Absolute Return. Andy Golden, retiring CIO of Princeton’s endowment, managed the Absolute Return portfolio for Yale. There was no capital introduction. They had to know that the Absolute Return industry existed and had to have the governance structure to allow the team to explore the opportunity. In 1995 or 1996, Swensen and Dean Takahashi went to New York and met a manager called Louis Bacon, who managed over $1 bn, but nobody knew. He started Moore Capital in 1989 with $25,000 he inherited from his family. By simply being earlier gives unfair advantage to build relationships with those managers.

In mid-90s, Absolute Returns managers became under limelight. George Soros and Stan Druckenmiller’s victory over the Bank of England in 1992 was well covered by the media. Before 2020, Tiger Management became the largest hedge fund manager with $20 bn. The industry was no longer secret. At many institutional investors poured capital into the industry, it became very crowded. Many hedge fund managers became rich, not necessarily because of the performance, but asset growth. Their 2/20 model generated more money than they ever saw before. In 2008 letter, Swensen add an unusual passage:

An important attribute of Yale’s investment strategy concerns the alignment of interests between investors and investment managers. To that end, absolute return accounts are structured with performance-related incentive fees, hurdle rates, and clawback provisions. In addition, managers invest significant sum of alongside Yale, enabling the University to avoid many of the pitfalls of the principal-agent relationship.”

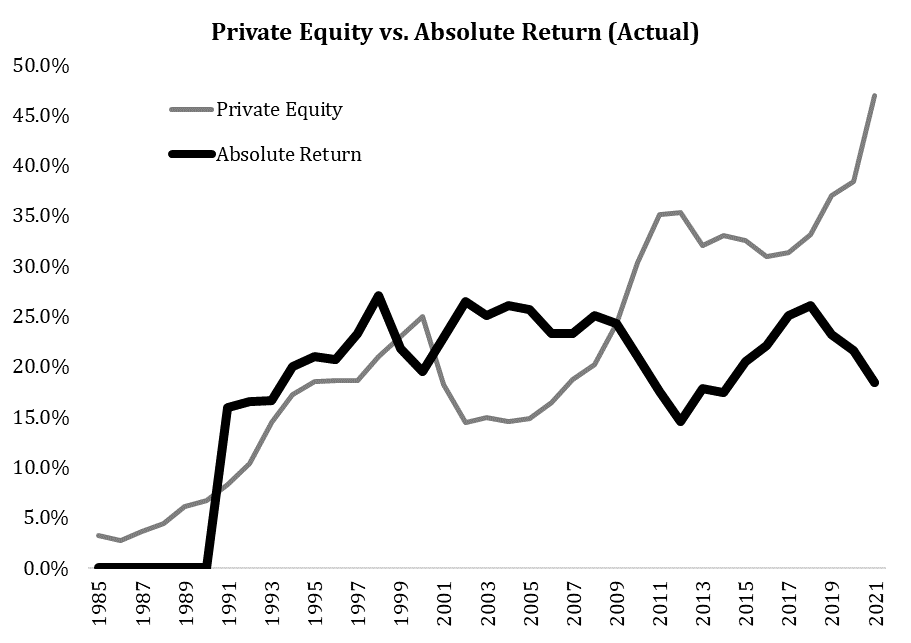

Many educational investors followed Yale and increased allocations into Absolute Return and maintained high rates of allocation as Absolute Return proved the benefit of downside protection in 2008/2009. On the other hand, Yale started reducing the exposure to Absolute Return as they were worried about the alignment of interests and the extremely low interest rate environment. Other asset classes, such as Venture Capital and Leveraged Buyout, became far more attractive than Absolute Return.

Yale’s outperformance is not a magic, but driven by their unconventional asset allocation. Absolute Return is just one of many examples of how Yale acted differently from other institutional investors. Many investors are still trapped by the Efficient Market Theory, which forces you to have the market portfolio that doesn’t exist. Even if it does, it forces you to overweight to the markets and sectors that have outperformed.

John Maynard Keynes famously said, “it is better for reputation to fail conventionally than to succeed unconventionally.” Would you dare?

Read previous posts:

Fall 2023 Letter

Dear Friends and Families, I trust that this letter finds you well. Company Update We are pleased to announce that we have a new member to the House of Mulans. In April, we started our search of a new colleague in Singapore and reviewed 136 applicants. We spent the following 4 months to find the right person. It certainly took longer than we anticipated, b…

A Young Allocator’s Checklist of Psychological Biases

Intro Disclaimer: Your writer (CHAN Yong) recently joined Star Magnolia and prior to that was navigating the world of capital allocation while investing for his family. While views and investment-related examples expressed in this article are in sync with Star Magnolia Capital’s investment philosophy, they are wholly from your writer’s personal investmen…

This post is so interesting, and really made me think.

Since most of the celebrated, iconic hedge funds started before they were treated as an asset class by institutions, and the consensus view is that most HFs perform less well than the market, would you say the "institutionalization" of the source of capital for HFs has some impact on the asset class's overall under-performance, while only large multistrat firms, e.g. Citadel, Point72, which are a subset of the asset class have performed well? Putting it differently, if you were to start a more classic, stock-picking hedge fund today, drawing lessons from history, would it be best to delay institutional funding for as long as possible, if the goal is out-performance not asset accumulation?