Leaping toward People’s “Liberated” Currency

“We need banking but we don’t need banks anymore. Do you think someday we can open bank account or ask for loan without physically have to come to the bank?”

Bill Gates, Founder of Microsoft

Disruption in Banking

After the 2008 financial crisis, many banks were reluctant to lend to consumers and small businesses due to internal capital ratio concerns, increased regulatory restrictions, credit/liquidity risks, and lack of profitability. To cover their high operating costs and inventory risk, banks had to charge a higher interest rate for both cash loans and lines of credit.

Thanks to advancing technology, a new type of banking service, social lending (aka P2P lending), has entered the market. Reaching consumers via interactive websites, social lending companies serve as a more efficient, low-cost digital platform. They connect borrowers and lenders seamlessly to provide cheaper and faster credit in an automated and user-friendly way. These sites refine the labor-intensive, standard methods of credit assessment by using an algorithm to analyze credit scores along with behavioral, social, transactional, and employment information of the borrower. These nuances allow the social lending platforms to offer borrowers lower rates than those by traditional lending methods. It is truly a win-win for both constituents: borrowers receive financing at a lower rate, while lenders receive a yield higher than that of comparable debt instruments. Social lending, while still a small fraction of the total consumer lending, is growing exponentially from a small base (Exhibit 1).

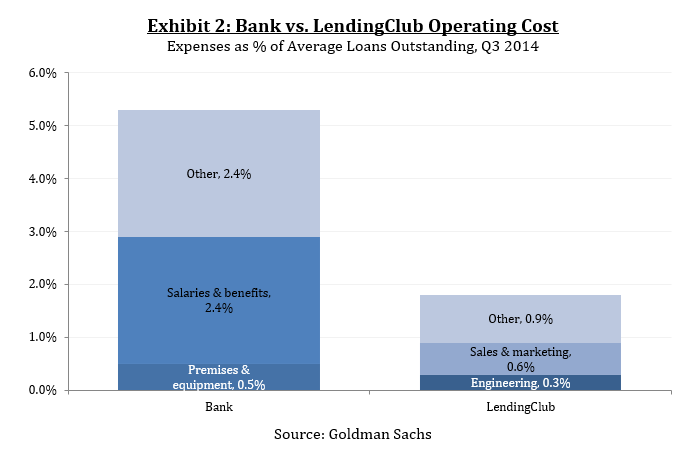

Social lending has advantage over the traditional banks in its low cost structure. While traditional banks spend more than 5% of the loan amount to originate itself even in the current zero interest rate world, the new age lenders can reduce the cost by more than 60% (Exhibit 2) by eliminating the costs of physical banks and human tellers.

In the near term, we expect US based social lending platforms, such as LendingClub, to grow by expanding its spectrum of borrowers, investors, and product offerings, as well as to grow by expanding into new geographies and M&A. In the long term, PwC predicts that the P2P lending market will exceed the peak of standard consumer finance loans outstanding by 2025, reaching $150 billion or higher.

Crouching Bankers, Hidden Opportunities 2

While social lending is powerful in the US, it is much more disruptive and powerful in China. As we discussed extensively in our previous letter, Crouching Bankers, Hidden Opportunities, the banking system in China is highly inefficient with little regulation, while its shadow banking system is already large and growing. Banks in China are generally unwilling to issue personal and small business loans; thus they primarily lend to state owned enterprises, which is driving the shadow banking’s growth. Therefore albeit the fact that the non-bank, micro loans have existed for several decades, more than 78% of Chinese people still do not have access to credit, according to the People’s Bank of China (PBOC).

In fact, China has already become the world’s largest social lending market. The number of social lending platforms in China exploded over the last five years (Exhibit 3), and its outstanding lending balance is already more than three times that of the United States (Exhibit 4). Given China’s massive internet population and expansion of mobile payment system, its disruption potential is significant.

The largest social lending operator in China is called Lufax, a subsidiary of Ping An Insurance, which is one of China’s largest insurance companies. Lufax has a risk management team of 100 people, an IT department of 200-300 people, and a platform of 7.5 million registered users. The valuation of Lufax, as reported in the latest round of capital raising, exceeds US $10 billion, which is bigger than LendingClub’s US $7.5 billion valuation (as of March 23, 2015).

Another player in the social lending market is China Rapid Finance, which recently announced that it had extended pre-approved loan offers of RMB 500 (approximately U.S. $80) to 50 million consumers through Tencent’s QQ social networking platform with 820 million users. On the other hand, the company has also teamed up with China Union Pay to screen creditworthiness of the borrowers. Considering China Rapid Finance only originated 300,000 loans in 2014, its current attempt seems disproportionately aggressive; and yet it demonstrates how those social lending platforms can reach out to a massive population, both instantly and inexpensively.

While the proliferation of China’s social lending platforms indicates that the market mechanism is finally functioning in China’s banking system, China does not have a well-established consumer credit scoring system, such as FICO in the United States; thus credit assessment in China is currently more of an art than a science. To attract investors, China’s social lending platforms often provide a guarantee and are thus vulnerable to credit risk. According to a research company called Yingcan Group, 275 of the P2P platforms (out of 1,575) either went bankrupt or had difficulty repaying money in 2014. Dagon Global Credit Rating Co., China’s leading rating agency, released a list of more than 350 of such platforms, which had significant credit risk. As competition intensifies and default rates increase more and more, small and weak players will face difficulties, and consolidation in the industry will follow.

Is social lending another “wealth management product”? Potentially. However, unlike the wealth management products, many of which were used to fund local government infrastructure projects, social lending addresses the bottleneck of China’s banking system – its mechanism of setting interest rates. The social lending platform allows its borrowers and lenders to arrive at a fair level of interest rates, which in turn, is paving the way to a more important reform of China’s financial system: the liberalization of Renminbi.

Leaping toward People’s “Liberated” Currency

In November 2012, Hongbin Qu surprised market participants with his bold outlook of RMB, which is to become convertible by 2018. In his report titled China’s Big Bang, Hongbin said:

The experiences of other countries show that the road to financial reform, especially capital account liberalisation, tends to be a bumpy one. To stay on track and to avoid major distortions, China must get the sequence of the reforms right, that is, to strengthen its domestic banking system, liberalise interest rates and develop a functioning bond market before making the RMB convertible.

Liberalization of interest rate setting mechanism is a critical prerequisite for the liberalization of RMB (Exhibit 5). Three key steps to liberalize the interest rates in China are: (1) establishing a deposit insurance system, (2) removing the floor for a loan interest rate, and also (3) removing the ceiling on a loan interest rate. Qu expected that these reforms can be achieved within three years of his report.

The Chinese government followed Qu’s prediction with amazing precision. In July 2013, the PBOC announced that it would eliminate the lower limit on lending rates offered by the nation’s financial institutions. In December 2014, the PBOC also unveiled the deposit insurance scheme, which is to become effective in the first half of 2015. Furthermore, they recently proclaimed that the deposit-rate cap could be removed this year if there were an opportunity to do so. Consequently, the biggest obstacle for the liberation of the people’s currency, or renminbi in Chinese, is likely to disappear soon; and the currency may even become fully convertible before Qu’s ambitious target.

As a World Payment Currency

Despite the lack of full convertibility, RMB has started gaining a significant market share as a world payment currency since 2008: when the government announced a pilot scheme of RMB cross-border trade settlement with Hong Kong, Macau and ASEAN countries and established offshore trading hubs in 14 countries and regions. Today RMB has become the fourth biggest world payment currency according to SWIFT, only behind the USD, EUR, GBP and JPY, from an almost nonexistence in 2012 (Exhibit 6). If transactions not captured by the SWIFT (e.g., trades across Sino-Burma border) are included, RMB’s market share may have already surpassed JPY’s.

From China with Capital

The ongoing financial reforms in China have significant implications for both domestic and foreign investors. More and more capital will be allocated away from the SOEs and toward the high-growth SMEs, which will boost the long-term economic outlook of China. At the same time, excess capital in China will be invested overseas. As Exhibit 7 below shows, China’s status as a net importer over the last 30 years is about to change, although it is still the largest receiver of foreign direct investment. Once the restriction on cross-border capital transfers is lifted and the currency becomes fully convertible, the trend of China’s outward investments will further accelerate.

Historically, Chinese investors have been more interested in resources and real estate-related investment. However, as the Chinese economy matures and people demand more for a better quality of life increases, the target industry of Chinese investors is shifting from commodities to high technology and financial services (Exhibit 8).

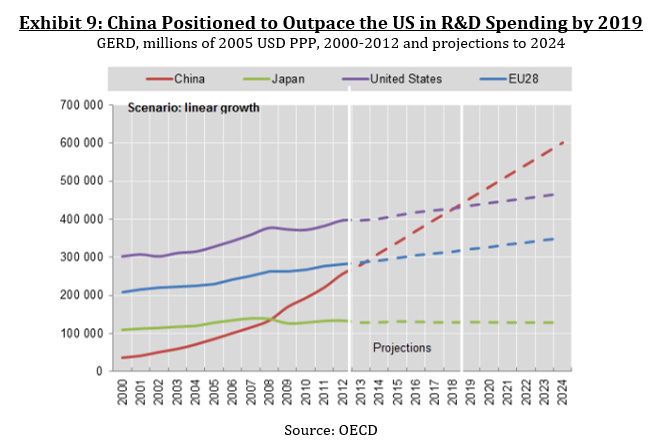

Although China is positioned to become the world’s largest R&D spender in 2020-2025 (Exhibit 9), it still needs more intellectual properties to satisfy its growing domestic demand. Acquiring foreign companies with advanced technology is a faster, and probably, a cheaper way for many Chinese companies.

Conclusion

China’s banking and currency reforms will have a major impact on our investment decisions over the coming decades; and yet, the potential consequences of such reforms are not receiving adequate attention. We think that the liberalization of RMB will happen in the next three to five years, if not earlier.

We conducted research on the development of P2P lending jointly with Cook Pine Capital LLC.