In the Mood for Speculation

Kennedy Town

We moved from NY to HK in June and have finally found a comfortable flat with a big patio (which we have quickly populated with fruit trees for self-sustenance) in Kennedy Town - the northwestern part of Hong Kong Island, where the construction for a new subway station is underway. Expecting the price increase in the area, real estate buyers and brokers are flooding into this neighborhood. Today, more than 40 property agent offices sit shoulder to shoulder on a 0.6-mile long main street (Belcher’s Street); of which, 16 offices fighting in the most congested block in front of the Westwood Mall (see Exhibit 1). However, Kennedy Town is not a special case: this real estate craze is just about everywhere in HK.

Fourth Year of Expansion

HK’s residential real estate market is seeing the fourth consecutive year of annual growth. Similar to NY and London, HK experienced a steady increase in the real estate price from 2003 to 2006, but the steady growth period was halted when the global financial crisis hit. However, HK’s real estate market rebounded, stronger than ever, and its growth and its price increased almost 80% from 2009, while NY’s real estate price fell more than 10% (See Exhibit 2).

In the Mood for Speculation

There are good reasons why HK’s real estate price has continued rising. With few better alternatives to invest their money, mainland Chinese buyers have kept driving up the residential prices in HK - their transactions representing over 30% of all purchases by value according to CLSA. Because of HK’s fixed exchange rate policy, the interest rate is kept low. As a result, local homebuyers can borrow money at a rate, which can be as low as 2.0% for 30-year mortgage. For most HK households, real estate investment is the largest component, and their strategy has worked quite well. Thus, you often hear “Hong Kong’s property price won’t go down. It’s a perfect hedge against inflation.”

During our apartment search, we have realized that renting an apartment in HK is actually quite affordable, compared to purchasing it. It depends on the property type and location, of course, but an average rental income yield is only 2.5% to 3.5% for most properties. I suspect most of the new landlords are cash flow negative, after considering vacancy, mortgage payments and other expenses. After adjusting for inflation, HK’s Real Rental Yield (gross rental income divided by market price, adjusted by inflation) is lowest among the three cities listed above and Tokyo. It is notable that the high-end properties in The Peak is yielding -1.67% after inflation, which implies that the investors are ONLY expecting a price increase.

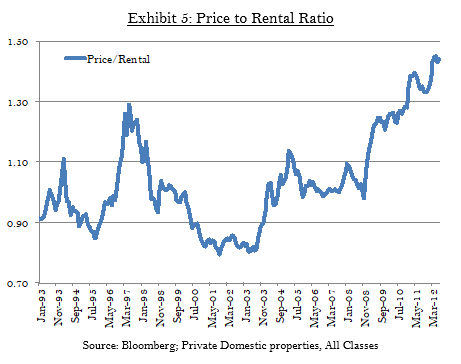

As shown in Exhibit 4, the residential rent level is not growing as fast as its price. After adjusted by inflation, HK’s rent level has not increased for the last four years. Exhibit 5 shows that the price-to-rent ratio is far above 1997’s peak level. We observed a similar phenomenon in the United States in 2007 and in Japan in 1989, a textbook example of speculation.

The Biggest Hedge Fund Investor in Hong Kong

A director of the investor relation of a NY-based hedge fund visited HK this summer. At our meeting, I asked him who were the most active institutional investors in hedge funds in HK. His answer was interesting – Hong Kong Monetary Authority (HKMA) and The Hong Kong Jockey Club. The Hong Kong Jockey Club, founded in 1884, is the largest taxpayer in HK and is a pioneer in hedge fund investing in Asia with over 10 years of track record and $8 billion AUM. The Jockey Club makes money as its customers bet on horse races and makes even more money as it bets on hedge funds. This makes sense.

How about HKMA? It is the de-facto central bank in HK, setting the policy interest rate and managing its current policy. HKMA implements the currency peg operation by selling HK dollars and purchasing US dollars when the exchange rate hits the upper trading range. Its Foreign Reserve account is growing helplessly over the last 4 years, almost doubling its size (Exhibit 6). It has publicly stated that it holds far more assets than it is normally required to protect the currency regime. HKMA seems to have half-desperately chosen to invest in hedge funds instead of expensive US Treasuries.

Unsustainable Currency Peg

Last week, HKMA announced that it sold over HKD 14 billion to protect its currency peg for the first time in the last three years. The capital continues to flow into HK and to push up the real estate price. The HK government initiated many efforts to cool down the housing market, including a new 30% tax on purchases by foreigners and a restriction on mortgages for luxurious properties. However, neither is having a real impact. The revaluation of HKD seems to be the tool to solve this problem.

Pershing Square’s Bill Ackman disclosed its position for HKD, which anticipates a 30% increase against USD. Ideally, HK dollars should be pegged to Chinese yuan as overall trade with the mainland now accounts for 50% of the total (US is only 10%). However, the Chinese yuan’s lack of convertibility poses a difficult hurdle. I think long HKD works very well with short JPY, given my pessimistic outlook for my home currency. I will elaborate my views on Japan in the next letter. Stay tuned.