Global Market Monitor: 2023 Review and Known Unknowns

Global Market Monitor: 2023 Review and Known Unknowns

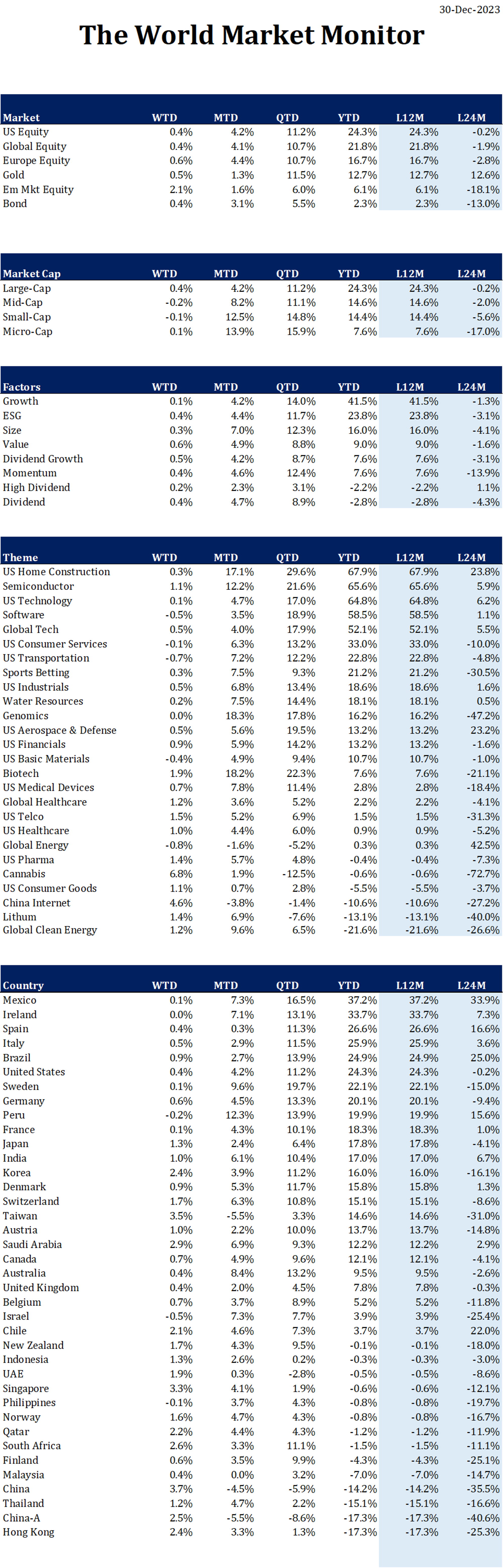

The global financial market closed a stellar year after a disappointing 2022, but we should review the performance of the market carefully as the devils are in the details.

There are a few important observations.

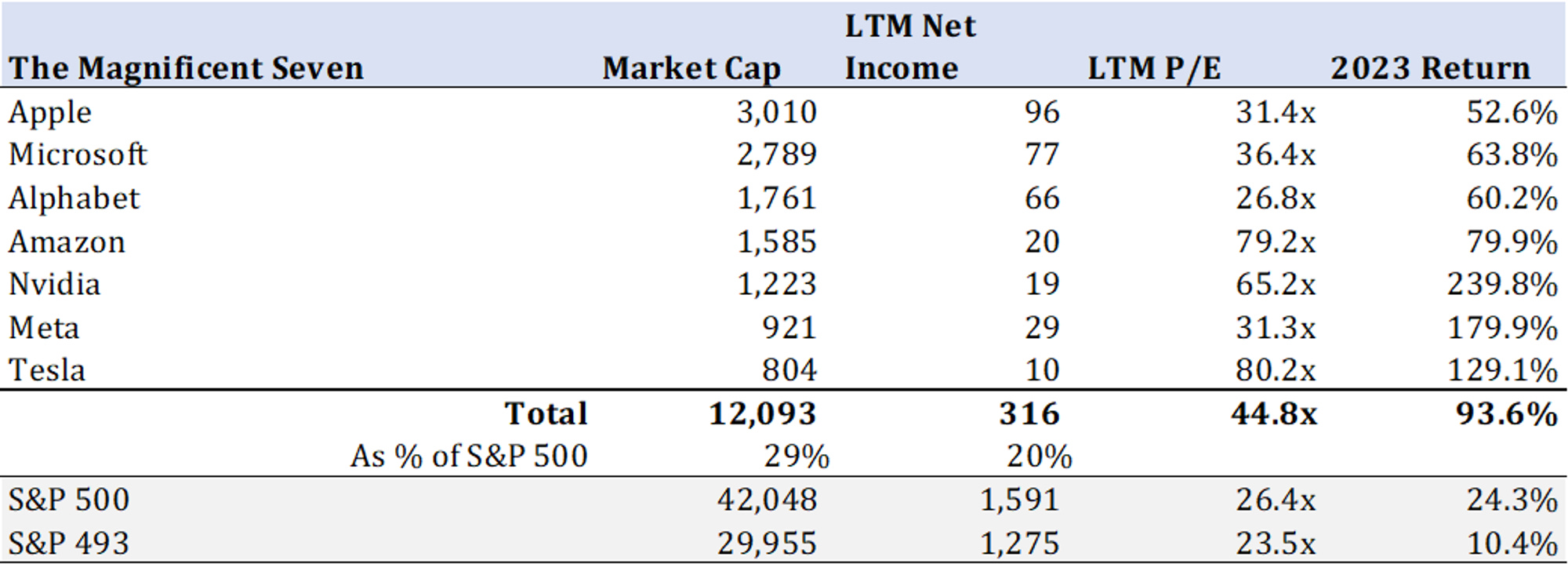

The Magnificent Seven vs. The Ordinary 493

It was the year of US Large Cap (up 24.3%)… actually, it was the year of the Magnificent Seven, which collectively represent 29% of S&P 500’s market cap. Magnificent 7 is up 93.6% this year. It’s almost impossible to beat this return if you invest outside of The Magnificent Seven.

The Magnificent Seven is now trading at 44.8x P/E. The most expensive stock is Tesla, trading at 80.2x, followed by Amazon at 79.2x. The cheapest stock is Alphabet at 26.8x.

S&P 500’s P/E is now 26.4x. It’s definitely not cheap. You may wonder if the Magnificent Seven is lifting the overall valuation. You are partially correct. S&P 493 (excluding the Magnificent Seven) is still trading at 23.5x.

Small is Not Beautiful

The dispersions among the different market caps is growing as MSCI USA Large Cap Index generated 9.0% p.a. vs. Mid Cap and Small Cap’s 4.4% p.a., however, it doesn’t mean Mid Cap and Small Cap companies are materially cheaper than Large Cap companies (P/E ratios are 24.3x, 21.5x and 24.6x).

Buy Japan, Sell China

Everybody dumped Chinese shares, even local Chinese. Both Hong Kong and China-A (local markets) are down 17.3%.

Many institutional investors are allocating capital to Japan. In fact, in the local currency, Japan had the best stock market since 2013.

When you invest in Japan, it is important to consider hedging JPY. Since 2011, Nikkei 225 advanced 10.4% p.a. in JPY, but only 5.4% in USD. Almost half of the returns diminished due to the currency decline.

Interestingly, this result resembles what happened to India. S&P BSE Sensex’s local return of 11.0% p.a. was halved by the declining Indian Rupee.

Known Unknowns in 2024 (Politics)

The election calendar of 2024 is unusually busy, creating a lot of uncertainties.

We should carefully monitor the outcome of the Taiwanese presidential election on January 13. At this point, the polls are too close to tell. The market assumes that the incumbent DPP’s Ching-te LAI is going to win and continue the same pro-US, anti-China policy, however, the market has not priced in the “risk” of the victory of KMT’s Yu-ih HOU. If KMT takes the presidential seat, Taiwan’s foreign policy may change 180-degree and the risk of escalating the China-Taiwan conflict will diminish. In this case, what will happen to the US-China relationship? Nobody knows.

Indonesian general election is always messy and nobody wants to make any new projects until the result is out, so the economy is not moving as quickly as it should be. We still do not know what the likely outcome of the February election is, but it will be as polarized as the last one, but probably not as exciting as the election when Widodo won in 2014. The frontrunner is 72-year-old Prabowo Subianto. He will be challenged by Anies Baswedan (42 years old) and Ganjar Pranowo (54 years old). No matter who wins, Indonesia will become less exciting from a political perspective.

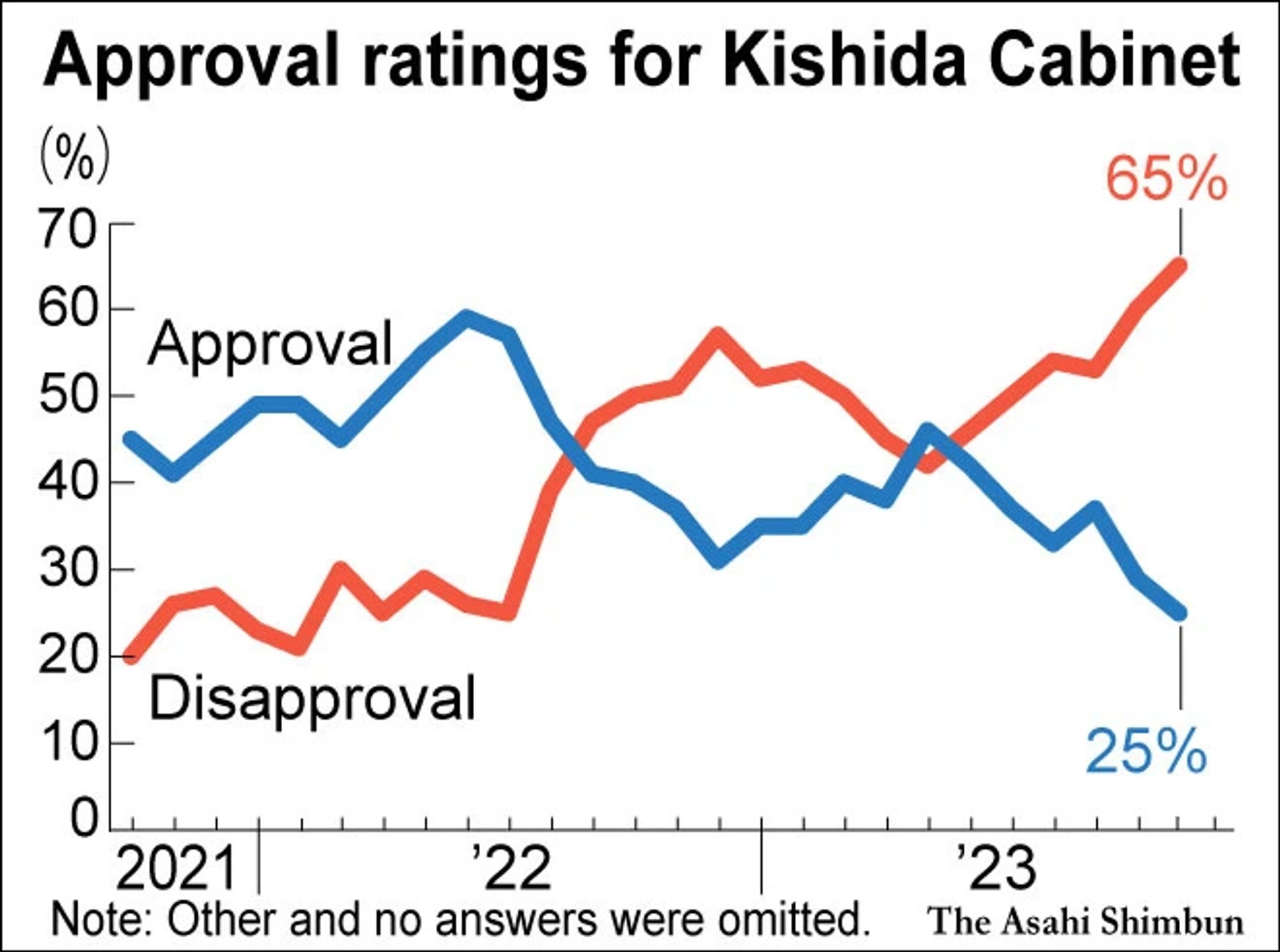

We should also monitor the popularity of the Japanese prime minister, Fumio Kishida. He keeps the post only because nobody from LPD wants to take the spot right now. If the political turmoil continues and the government cannot provide additional economic stimulus packages, it will become increasingly difficult for BOJ to increase the interest rate. In this case, the Japanese yen will start the losing streak again in 2024.

About the Author

Shinya Deguchi is an allocator at Star Magnolia Capital. He is responsible for the company’s management, research, and family relations. He joined Star Magnolia Capital in 2012 after working in the United States for 8 years. Most recently, he was Director of Research at Cook Pine Capital in Greenwich, CT where he assisted Mr. Eiich Kuwana on the company’s investment-related activities. He was born in Japan and graduated from George Washington University in 2003. He enjoys reading manga.