Crouching Bankers, Hidden Opportunity

“Everyone is talking about credit – about the credit cycle, leverage and credit-quality problems. It’s a big black box, and it’s quite scary.”

Stephen Green, Head of Greater China Research at Standard Chartered

The summer shockwave that hit China’s interbank market this year served as a rude awakening to all participants. Both Bank of China and China Everbright Bank were beset by rumors of a serious liquidity crunch. The two ended up issuing very public denials that they were in any danger of a cash shortage. A full-on crisis was finally averted as the People’s Bank of China (PBOC) injected liquidity into the market and signaled a willingness to establish a deposit insurance system. However, Chinese banks took away a hard-earned lesson: PBOC was ready to shut down the entire banks and bring the flow of credit to a screeching halt in order to curb irresponsible lending.

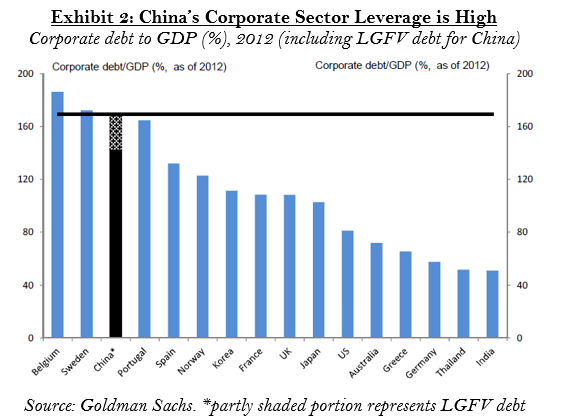

The center stage of PBOC’s concern was China’s high and rising corporate leverage. With a debt-to-GDP ratio of over 200% and the majority of it within the corporate sector, the central bank’s concern is warranted. According to Goldman Sachs, China’s corporate debt ratio is among the highest in the world (Exhibit 2).

The emergence of the alternative (i.e., non-bank) financing also caught worrying investors’ attention as it grew from 20% to 50% over the last five years and now represents 30% of the overall credit balance (Exhibit 3). Historically, the supply of credit in China has been channeled mostly via the banking system, but many of smaller companies have been crowded out of the bank loan market, and this led to the rapid development of shadow banking as companies seek out alternative funding routes.

However, what shadow banking really is as confusing and misleading. The term shadow banking implies that these activities operate illegally, irresponsibly and completely outside regulatory supervision, but that is not accurate. In fact, China’s shadow banking system represents both bright and dark sides of China’s financial system.

The Dark Side of the Shadow Banking

The local governments launched a massive series of infrastructure development projects in 2009 as orchestrated by the central government to save the economy from faltering. Due to legal restrictions to borrow directly, the local governments channeled their borrowings through Local Government Financing Vehicles (LGFVs) and, as a result, their financing activities surged by more than 100% (Exhibit 4).

Not surprisingly, the lending standard for the LGFVs were low; Goldman Sachs’s analysis on 470 LGFV bond issuers found that 42.6% of those issuers had negative free cash flow in 2012 and most of them were not expected to generate sufficient cash flow in the near future. Sponsoring local governments are providing implicit guarantees for LGFVs, but they are also facing a structural problem. The local governments are responsible for providing both infrastructure and social welfare for urban citizens and, as China’s urbanization accelerates, the burden for the local government has increased without securing enough funding sources. The local government is responsible for 83% of the national expenditure, but they are entitled to only 66% of tax revenue (Exhibit 5). In 2012, over 20% of the local governments’ total revenues were generated from land sales, which is non-recurring. This model is apparently not sustainable, and the central government is fully aware of it. In June 2010, the National School of Development “surprised” the world after it announced that an estimated 24% of these loans had “severe default risk”.

Alibaba, the Micro Lender

“No collaterals, no secret connections. What we need is your credit.”

Jack Ma, founder and former CEO of Alibaba

Alibaba is a Chinese e-commerce company, started by Jack Ma in 1999. This company, which started as a business-to-business portal to connect Chinese manufactures with overseas buyers, became the world’s largest online portal with $170 billion in sales, more than eBay and Amazon combined.

In Jun 2010, Alibaba started a microloan business with an aim to support its customers, which are predominantly small private companies. According to a survey conducted by Alibaba Group and Peking University, relatives and friends were the main sources of funding for the small and micro enterprises (businesses with an annual turnover of less than 30 million yuan). Less than 30% of the 10,446 businesses, which were surveyed between May 2011 and May 2012, raised funds through banks. Over the last three years, Alibaba has extended more than 100 billion yuan of financing to over 320,000 small online businesses and entrepreneurs. Given China’s outstanding microloan balance of 592 billion yuan, Alibaba represents at least 10% of the market. The average size of Alibaba’s loans is 40,000 yuan.

Alibaba’s advantage is its access to the data of underlying borrowers, who are conducting businesses on Alibaba’s platform, and therefore, Alibaba can make an informed decision in a far more sophisticated way than other financial institutions. Although Alibaba charges 18.9% a year for these non-secured short-term loans on average, the customers’ demand had been high because the growth of their businesses was strong enough to cover the high interest payments. The non-performing loan ratio was only 0.87% as of the second quarter 2013.

Small Loans, but Not-So-Small Efforts

One way that the government has sought to increase the efficiency of capital allocation is through tacit approval of the Small Loan Companies (SLCs), licensed by the provincial-level governments to originate loans to small businesses (Exhibit 6). Due to the tightened lending restrictions on property developers and small private businesses, SLCs are functioning as an effective loophole in the regulatory framework – injecting liquidity into the financial system.

For secured loans with 2-3x collateral coverage, it is not unusual to find deals with rates of return in the mid to high teens. Most importantly, the critical difference of the shadow system versus the established banking system is that rates are set by the market’s demand and supply. One of the positive developments is the government’s willingness (at all levels, central and local) to accommodate foreign capital in order to shore up China’s inefficient banking system. Among provincial governments, Chongqing municipality was particularly successful in attracting prominent foreign institutions, including Singapore’s Temasek Holdings, to establish local SLCs. In addition, at least two asset management companies (AMCs) in China are seeking to raise capital in the overseas market. These are the same institutions that played a critical role in cleaning up bank balance sheets during the previous financial crisis in China, thereby setting the stage for the IPO of the Big Four banks.

The Real Meaning of the Shadow Banking

For China, what shadow banking really means is a free interest rate setting mechanism based on the supply and demand. China’s banking system is so bureaucratic and inefficient, if not corrupted, that commercial banks have very little incentive to extend funding to the smaller private businesses, although the private sector is now contributing over 60% to China’s GDP, according to the All-China Federation of Industry and Commerce. Both Alibaba and SLCs are just trying to narrow the gap commercial bankers cannot fill.

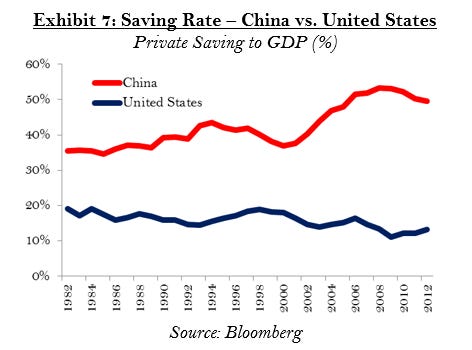

Another big problem for China’s banking system is the lack of alternative investment options for savers. The saving rate in China is quite high (Exhibit 7), but the bank deposit rate is controlled and set by the government, ranging from 0.35% (current) to 4.75% (5-year), in order to protect bank’s profitability. As real interest rate is close to zero after adjusting for the high inflation, a better investment solution was seriously needed for the Chinese savers and their answer was wealth management products (WMPs).

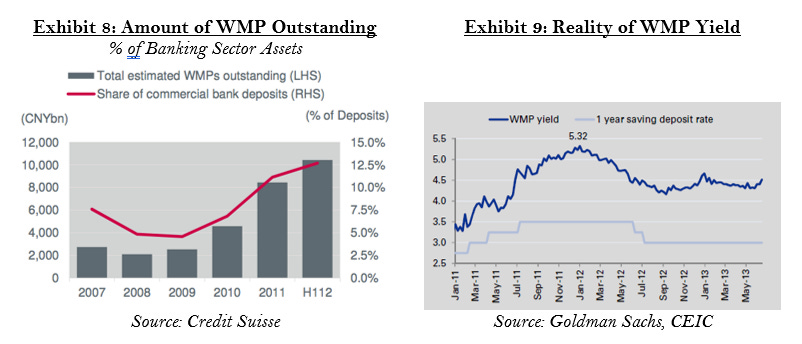

The WMP industry grew very quickly since 2009 and its balance already reached 12.5% of total deposit of China’s banking system (Exhibit 8). WMPs are, in essence, capital raising channels of the shadow banking and are criticized as a poster-child of China’s irresponsible lending activities, after some misinformed bankers sold the high risk WMPs as if they were guaranteed by the banks and investors were very upset when they learned that they lost their life savings. While it is true that there are many questionable WMPs “promising” above 20% returns, the average yield of WMPs is only 3.5-5.5% (Exhibit 9). I think the risks associated with WMPs were somewhat exaggerated.

Crouching Riskers, Hidden Opportunities

“The things we touch have no permanence. My master would say: there is nothing we can hold onto in this world. Only by letting go can we truly possess what is real.”

Li Mu Bai, Crouching Tiger, Hidden Dragon

The new government is making efforts to reform China’s financial system, having already taken several important steps, such as removing minimum lending rate. Recent announcement to establish a deposit insurance system, like FDIC in the United States, will allow the government to close down troubled banks. The next step is the liberalization of the deposit rate. The commercial bankers are fiercely opposing to this new policy as it means their funding cost will increase.

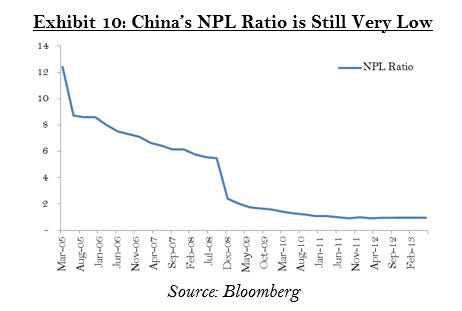

On paper, Chinese bank balance sheets are among the world’s best. Their capital adequacy ratio was 9.9% at the end of June, higher than both the 9.5% rate required by year-end 2013 under Chinese Basel III requirements and the 8.0% level under global Basel III directives. Furthermore, less than 1% of the total commercial loans were marked as non-performing (NPLs) as of June, according to the China Banking Regulatory Commission, China’s main bank regulator (Exhibit 10).

As is often the case with Chinese bank statistics, a closer look reveals a surprisingly different picture. The year-over-year growth of NPLs was 18.2%, in line with the 17.0% in overall loan growth, but this was due largely to the outperformance of loans originated by state-owned Big Four banks, which account for 60% of the total outstanding issues. The same figures for smaller banks were 39.8% and 29.0%, respectively, indicating that the rapid growth of NPLs far surpassed the speed of loan origination. Considering the Big Four’s balance sheets are dominated by loans to state-owned enterprises (SOEs), the definition of NPL loses much of its meaning. SOEs by definition will never be classified “non-performing” lest there is a loss of implicit government support. As a result, despite deteriorating credit quality, NPL ratios of large nationally-owned banks were growing at far lower rate than that of smaller banks (Exhibit 11).

After the real estate bubble, it took seven years for the Japanese government and financial industry to admit the scale of NPL problem. In 1992, Japanese financial institutions estimated that the NPL ratio should peak at 1.13%, but it eventually hit 8.4%. From 1990 to 2006, 181 financial institutions were shut down and the total number decreased from 1012 to 582 as a result of mergers for survival.

Goldman Sachs estimates that the worst-case scenario for Chinese credit losses could reach $3 trillion, greater than the GDP of France. The Chinese government is worried that the problem has grown too big, too quickly, and now offering foreign capital a chance to clean up the country’s balance sheet. This in fact presents some potentially lucrative investment opportunities to those who can afford the risks.

The real economy is growing rapidly and is creating a solution (i.e., shadow banking) to support itself. The only thing the government should do is to let the market decide what is best for it; otherwise, the problem will grow out of control. Based on my observations and conversations with the experts, the government is quite serious about the financial reform and willing to take pains with supports from overseas.

Our experiences from the S&L crisis in 1990s, Japan’s banking crisis in 1997, and the ongoing European debt crisis tell that the opportunity set to invest in NPLs could become very attractive for foreign investors with long-term capital and sufficient expertise. Currently, most of distressed investment managers are tied up with European situations and the lack of attention to China by overseas (and domestic) investors makes this opportunity set even more attractive. As old-fashion bankers are crouching, we can finally see the hidden opportunities in China’s credit market.