China 101010

Only buy something that you’d be perfectly happy to hold if the market shut down for 10 years.

Warren Buffett

Ride an Ox, Find a Horse

“Ride an Ox, Find a Horse (騎牛搵馬)” is a Cantonese proverb, meaning that one should do with what one can find (an ox), and then try to catch something better (a horse). In 2014, we enter into the Year of the Horse, and we are still missing bulls in the Chinese stock markets. The CSI 300 Index, which tracks 300 Chinese domestic shares, fell 7.65% in 2013, while both S&P 500 Total Index (up 32.39%) and Nikkei 225 (up 56.72%) had the best year since 1997 and 1972, respectively.

Without a doubt, China is in trouble as its banking system is facing mounting losses from irresponsible loans to the local governments, which soared 70% to almost US$3 trillion in less than three years. Chinese stock markets are still down 60% from the peak in 2007, and its pessimistic P/E Ratio valued at 11x is warranted: the banking sector represents 40% of the index. The only silver lining is the rapidly growing Internet companies like Baidu and Tencent. However, after an 87% surge in 2013 (CSI Overseas China Internet Index), China’s Internet stocks are no longer cheap as they are trading between 30-100x of next year’s earnings.

If this is what you think, you may miss a bargain on China’s crown jewels: a good opportunity exists exactly in these China’s old and “boring” businesses with recognized brands. Most of these brands have existed for more than 30 years - some of which even date back to the late 16th century - and they have become undeniably an important part of people’s daily lives.

China’s Non-Financial domestic equity markets, so-called A-shares, can be divided into two groups: there are approximately thirty Non-Financial Large-Cap companies (above US$ 10 billion) and over 2,200 Non-Financial Small-and-Mid-Cap companies (below US$ 10 billion). However, while the Small-and-Mid-Cap companies are trading at 66x P/E ratio, the Large-Cap companies are trading at 15x P/E ratio with 18% EPS growth expected for 2014. (Exhibit 1, previous page)

The performance of the Non-Financial Large-Cap companies’ business model is the proof of its resilience. Since 2002, the Non-Financial Large-Cap companies have returned 931%, while CSI 300 Index is up only 76%. (Exhibit 2) Even compared from the peak of China’s bull markets in 2007, the Non-Financial Large-Cap companies are down only 11% (CSI 300 Index is down 60%). Despite this apparent outperformance, these Non-Financial Large-Cap companies are still trading at near historic low P/E multiples. (Exhibit 3)

China Equity - Still Very Foreign to Foreigners

Why are China’s leading domestic companies so neglected by the investors? There are a few reasons: Firstly, the A-shares markets are still dominated by mom-and-pop retail investors, who are chasing short-term returns on hot stocks and so are not interested in these large cap companies, as their share prices move with less volatility. They rarely conduct fundamental researches; therefore, they do not understand the true value of the companies in which they invest. Secondly, although the combined market capitalization of China and Hong Kong stock markets represents 11% of the world, the foreign ownership is only 11.4%; and for China A-shares, foreign investors own less than 2%. (Exhibit 4) In short, the second largest equity markets are almost completely neglected by not only the domestic investors, but also foreign institutional investors. Without sophisticated investors who can make investments based on a long-term horizon and fundamental value analysis, China’s most valuable companies will continue to trade at very low valuations. Ah, an opportunity!

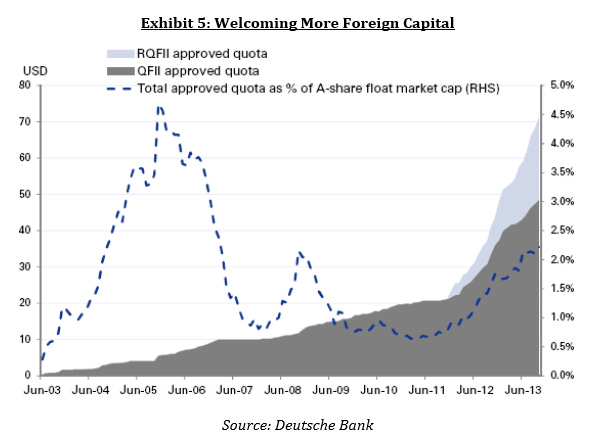

Currently, only qualified foreign institutional investors (QFII) can invest directly in China’s A-shares, and the requirement for this qualification had been very high until 2011. In order to encourage more foreign investors to own Chinese stocks, the government lowered its threshold in 2012 to minimum asset size from $2 billion to $500 million. China also increased the quota for RMB QFII (RQFII), a special scheme for HK-based asset management companies, from RMB 20 billion (US$ 3.3 billion) to RMB 270 billion (US$ 44.6 billion). As a result, the total amount of capital deployed to Chinese markets tripled from US$ 20 billion in 2011 to $70 billion in 2013. (Exhibit 5, next page) This trend is expected to continue beyond 2014.

The relaxed regulatory regime began attracting new types of investors into the A-shares recently. Over the last two years, the growth of QFII quotas for Banks and Brokers and Central Bank & SWF slowed down, while those for Insurance and Pension increased. There were also five alternative asset managers, i.e., hedge funds, which became QFII with a US$ 830 million quota. The most notable new investor is Alta Advisers Limited, a UK-based family office for Swedish billionaire Hans Rausing. It is still uncommon for family offices to become QFII by themselves due to the size of commitment (usually, the Chinese government expects QFII to invest at least $50 mm in A-shares).

On the other hand, you can still invest in China without becoming QFII, if you can “borrow” quotas from your brokers for 1-2% fees on the transaction amount, each way. These quotas belong to the brokers, so they can cancel the allocations before your investments reach the full valuations. The QFII rule will eventually become meaningless, as the government feels more comfortable with foreign investors and create more flexible ways for foreigners to invest in the A-shares. However, by then, the Chinese market will become more expensive as more foreign investors realize the attractive valuation.

Invest in China like Buffet Does

Warren Buffett, the best fundamental stock picker, bought most of his core long-term holdings, such as Washington Post (1973), GEICO (1976), Coca Cola (1988), Wells Fargo and P&G (1989), when the S&P 500 Index was trading at a discount, or below 14x. Buffet said: “only buy something that you’d be perfectly happy to hold if the market shut down for 10 years,” because it is more difficult to buy good companies at discount than at premium. (Exhibit 7, next page)

We like China’s rapidly growing Internet industry, but there are only a few Internet companies, which we can comfortably own for the next 10 years. Nonetheless, there are other names: many companies with established household brands, which Chinese consumers will continue to rely on for the next 10 years. For example, Chinese people will never lose their acquired taste for baiju, China’s white wine. As their living standard improves, they will drive more General Motors and buy more air conditioners to satisfy their needs. In today’s China, you do not need “bulls” to find great horses because horses are right in front of you. You are just not seeing them.

To illustrate how value investing works for a long-term investor, let me show a simple math. Suppose there are two companies, LargeCo and SmallCo. On January 1, 2014, they are trading at, respectively, 10x P/E with 10% average growth and at 40x P/E with 25% average growth for the next 10 years. After SmallCo’s growth period is over, both companies will be trading at the same multiple of 15x on December 31, 2023. A simple return from these two investments is 290% and 180%. It is, of course, possible to find even more attractive growth stocks and to achieve a better return. However, a good long-term investor should know which investment has higher probability to achieve this.

China 101010

Like Buffett, the best investment approach for a long-term investor is to have a concentration of companies, whose business models you fully understand. There are 10 companies we want to own for the next 10 years, which are trading at around 10x P/E for 2013. This is our China 101010 portfolio. The average growth rate from 2013 to 2015E of these 10 companies is 27.0%. Moreover, the average market cap of this portfolio is US$ 10.8 billion. Furthermore, if these 10 companies sustain this optimistic growth rate for the next 10 years, the value of the portfolio will be 10-fold. (1.27^10 ≈ 9.91). We love the number, 10, because in Chinese characters, doesn’t the shape of “ten” looks like a positive sign? (Exhibit 9)