Buy Low in Japan, Grow High in China

Japan is heating up among the institutional investors. Some say that there are a lot of opportunities in the undervalued public equity markets, and aggressive activist approach can unlock the value of corporate Japan. Some see opportunities in leveraged buyouts using the near-zero interest rate. What is common among these opportunity sets? Japan is cheap.

What is the catch? Well, buying cheaply does not guarantee good returns because the value of the company can go down if the company does not grow; and there has been just about no growth in Japan over the last and lost 30 years.

To make money, you need something more than buying cheap. For the activist approach in the public equity markets to work, you need a functioning corporate governance in place. The Japanese government did introduce the highly anticipated Stewardship Code in 2014 and Corporate Governance Code in 2015, but they were, again, just another half-hearted guidance without legal force. For whatever reason or lack thereof, both retail and institutional shareholders hate changes and abhor even more those instigated by foreigners, no matter how logical or rational they may be. Even after 400 years, Japan seems still traumatized by the horrifying memory of Commodore Perry.

In the case of a leveraged buyout, you need to borrow a lot of money and cut a lot of costs — usually by firing a lot of people — so that you can generate enough cash flow to pay the interests and have some leftover. Not surprisingly, firing employees is extremely unpopular and is fiercely opposed by different stakeholders — the employees, the government and even the banks — because no one wants to be the loser or the bad guy.

So, let’s think about another way of making money, other than firing people and antagonizing everybody. What is the alternative to cost cutting? Growth. If you can generate enough growth from the companies you buy, you do not have to penny-pinch in order to make a profit. Well, where is the growth, then? Right next door. Japan is sitting right next to one of the fastest growing economies in the world — China. China has the growing consumer market, which Japan lacks but needs; but Japan has a lot of attractive technologies and products, which China covets.

It is not like Japan has not realized this; in fact, Japan has been trying to cross the rough sea, just without much success except for a very few — e.g. Uniqlo, Muji and Pigeon. Japanese endeavor fails because when a Japanese company enters into the Chinese market, it invariably sends a Japanese management team, who has neither the knowledge nor the experience of the Chinese corporate culture. For example, they carry over Japan’s irrational compensation system where employees get paid according to seniority, not performance. However, in China, performance is everything and the top salesperson often earns more than the CEO.

China, on the other hand, has not been exactly solicitous, either. In 2015, the loosening of the restriction for tourist visa opened the floodgate of Chinese tourism. Since then, Chinese tourists have been “raiding” the Japanese stores and buying anything and everything, from rice cookers to diapers and the suitcases to take them home, crowding out the local shoppers and traditional merchants. When Chinese investors come to Japan to buy companies, they have the same attitude: they come with multibillion RMB in their wallet as if that were the license to disregard social curtesy and the local custom. Therefore, it is not a surprise that Japanese company owners refuse to sell their companies to those they regard, not as Chinese investors, but Chinese “invaders” regardless of the price.

Perhaps not in China, but Japanese companies have been exploring greener shores abroad, and their growing appetite has led cumulatively to a spending of $600 bn over the last 10 years in international M&A. However, Japanese enthusiasm has not been reciprocated: during the same period, foreign investors have largely stayed away from Japan, spending only $100 bn.

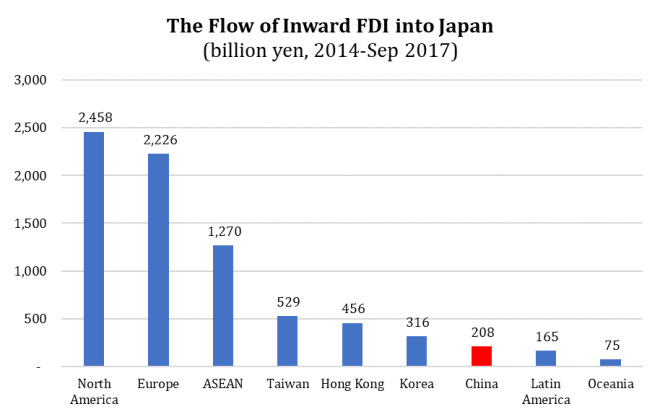

Zooming in on the inward foreign direct investment from 2014 to September 2017, the volume of investment activities from China to Japan is small, spending only JPY 200 bn in total, less than Taiwan, Hong Kong and Korea; yet this is the very period when Chinese investors bought many companies around the world. It is easy to surmise why there were not many deals: Chinese buyers had tried but failed to win over Japanese sellers. What a loss — to the Chinese and to the Japanese companies.

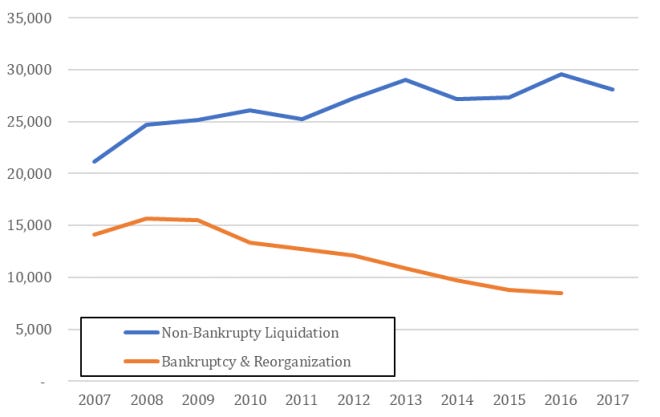

As we had discussed in our previous article, Corporate Japan’s Last 100 Years for the Next 100 Years, Japanese companies are aging, and very quickly, too. In 2016 alone, nearly 30,000 companies were liquidated for reasons other than bankruptcy, 3x more than bankruptcy and reorganization cases, and over 50% of these companies were in fact profitable.

More and More Companies Are Liquidated…

According to Japan Finance Corporation’s survey in 2016, 50% of the respondent companies with management aged 60 years old or above answered that the company business would be discontinued after their retirement, and nearly 30% said that their decision was due to the lack of a successor.

In 2015, Hagoromo Bungu, the world’s leading manufacturer of blackboard chalk, ceased operation after a long 82 years. The company sold 90 million chalks (30% of the domestic market) and generated more than JPY 200 mm (~$2 mm) revenue at its peak in 2006, but as the population of the schoolchildren declined, so did the domestic demand for blackboard chalk, and the company’s revenue fell below JPY 180 mm in 2014. The company owner explained that the main reason for the discontinuation was not the decline in revenue per se, but because the company could not find an appropriate buyer.

In 2017, Hakkeitei, a 130 year-old ryori-ryokan (auberge), closed its doors for the same reason. When the last chef-owner, Mr. Takenaka, became too ill, his two sons were not interested in taking over the family business. The historical building Hakkeitei would be handed over to the local government.

Okano Kogyo is a tiny manufacturer of metalworks, generating only JPY 800 mm (~$8 mm) in revenue in 2016. Despite its small size, it has over 30 patents, and most recently it has become world-renowned for making painless — or as painful as a mosquito bite — hypodermic needles. Okano produces the thinnest (3 micron) needle in the world, which it had developed in 2004 at the request of a large healthcare company for the diabetic patients. Nevertheless, the business will be shut down upon the present owner’s retirement as the owner could not find successors among the family members.

The difficulty of finding a successor arises not because Japan’s aging company owners are trying to keep the management control within the family, for they would rather see that the business they have spent a lifetime building is carried on even if it is by someone else. Therefore, the problem is not the intention, but direction because they have been looking at the wrong place — Japan. For Japanese companies, the best solution is to find a Chinese strategic partner, who has the market but lacks the technology or products. For Chinese companies, the best strategy is to acquire the majority stake in a relatively small Japanese company, which has advanced technology or unique products but is too small to expand into the Chinese market. From the perspective of the Japanese owners/shareholders, they not only have the peace of mind in having secured the jobs for their loyal employees, but they can also participate in the growth of their old companies through the minority stake. From the perspective of the Chinese buyers, they can operate the newly acquired business more efficiently as they can utilize immediately the knowhows of the continuing employees, with the added bonus of not having to worry about other meddling public shareholders.

On paper, it sounds perfect; but first the Chinese companies must be able to persuade the Japanese owners and to purchase Japanese companies. What has so far been blocking this synergistic, cross-border alliance is nothing other than mistrust. In order to dispel general misconceptions and to build trust, we need people who can communicate with both sides. Star Magnolia has been searching for such people to manage and execute this cross-border investment opportunity, and we have finally found the right people: they have the ability to communicate not just linguistically, but more importantly, culturally, and they can build the bridge over which Japan and China can indeed meet halfway and shake hands. “Buy Low in Japan, Grow High in China” is not another macro strategy: it is as micro as micro can be because we are making a bet on the people. After all, investment is all about people.