Analysis of Yale’s Manager Selection

Yale’s annual report is full of great insights. As we discussed previously, Yale generates 50% of outperformance from the asset allocation and another 50% from manager selection. Recently published 2017 annual report discussed extensively Yale’s belief in the active investment management and “unique” manager sourcing. I found the following quotes particularly important.

Source: Yale Investment Office, Berkshire Hathaway;

the performance period for Yale is ending June 30

and for Berkshire Hathaway is December 31

“Yale and other top endowments operate with a long time horizon. In his letter, Buffettwrites that institutions may be lured by the “siren song of a high-fee manager” and that “this year the magic potion may be hedge funds, next year something else.” While Buffett’s claims may be true of some poorly managed institutions, Yale’s prospective managers are thoroughly researched and carefully considered; manager hiring decisions are made with the hope of establishing enduring relationships. In fact, Yale’s manager turnover averaged 7.7% over the past decade, implying a thirteen-year holding period. Similarly, asset allocation decisions are not driven by the flavor-of-the-month, but by underlying asset class characteristics and opportunities. That decisions are influenced by the allure of a “magic potion” could not be further from the truth.”

“In advocating the adoption of a passive indexing strategy, Buffett provides sound investment advice for the vast majority of individuals and institutions that are unable (or unwilling) to commit the resources (human and financial) necessary for active management success. Yet, Buffett’s advice is not appropriate for the cohort of endowment that possess the capabilities to pursue successful active management programs.

“Long-term investment success begins with the identification of top-tier managers.”

“Start-up and early-stage firms play a central role in the Endowment’s sourcing process. While many institutions seek established managers with long-standing audited track records, Yale keeps an open mind to nontraditional firms and looks beyond standard metrics to assess the integrity and skills of investment professionals.”

Based on our interpretation, the following is common characteristics of Yale’s managers (of course, there are some exceptions):

High personal and business integrity

“Young and Hungry”

Employee-owned

Single strategy (not a platform)

Significant internal capital

High conviction, concentrated, long-term investment approach

Bottom-up, security-specific investment approach

No short-term trading

And, over the last 10 years (especially after 2013), Yale significantly outperformed its peers.

Source: Yale Investment Office

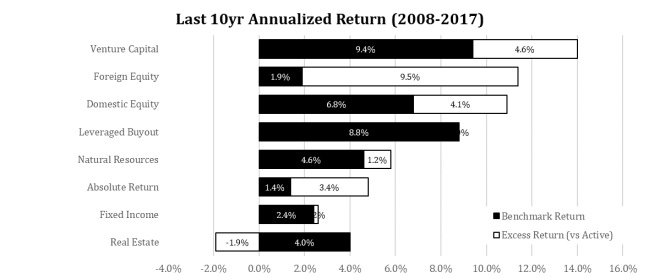

However, the outperformance is not coming from everywhere in the portfolio. The following calculation is not perfect as we are using the average allocation to reverse-engineer attributions, but our analysis shows that significant attributions were from three strategies: Venture Capital (16.4% avg. allocation), Foreign Equity (11.7%) and Leveraged buyout (8.8%). These three asset classes representing 43% of the portfolio generated 75% of the total returns.

Absolute Return

Yale allocated 20.5% of capital to Absolute Return, which has been an underdog with only 4.8% annualized returns, also played an important role to generate “excess returns”. Over the last 6 years, Yale drastically increased allocation to Absolute Return while its peers decreased.

Real Estate

Onthe other hand, Yale’s real estate portfolio performed quite poorly (2.1% p.a.) despite it was the second largest allocation for the portfolio (17.6% avg. allocation). Apparently, Yale is trying to reduce the exposure as fast as possible, but given the illiquid nature of the investments, it is taking longer.

Yale Investment Office Annual Report 2017