Analysis of Yale’s Asset Allocation 2017

Yale reported its 2017 performance (11.3%) and target allocation for 2017. The performance of the fiscal year 2017 was not as strong as its peers, but Yale’s long-term outperformance is still unbeatable. (source: YaleNews, Yale Investment Office)

Through June 2017

More Absolute Return (Hedge Funds); Less Real Estate

This is continuation of Yale’s asset allocation trend over the last 6–7 years

Note that Yale is not a good real estate investor — their performance is not as strong as other investments

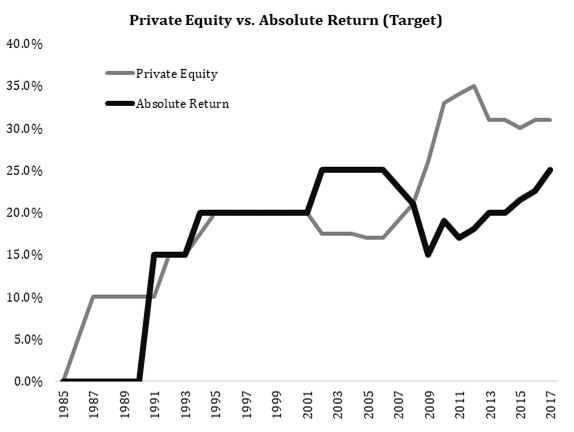

Private Equity Allocation Unchanged

The contrast between Private Equity and Absolute Return is obvious

Given strong performance of Private Equity, I believe Yale is taking profits from existing investments and not proactively adding to the new opportunities

More Venture Capital and Less Leverage Buyout

The increase of allocation is partially due to the increased value of underlying investments in Venture Capital

Other Notable Changes

Continuing reducing exposures to Real Assets (primarily Real Estate)

Doubling exposures to Foreign Equity over the last 6 years (mainly through Emerging Markets)

Maintaining relatively high cash and fixed income balance (better opportunities in the future?)