Analysis of Yale’s Asset Allocation 2018

Analysis of Yale’s Asset Allocation 2018

While schools have begun another year of learning, university endowments have just wrapped up their fiscal year ending June 30, 2018. Yale Investment Office reported that it had generated 12.3% return, bringing its performance over the last 20 years to 11.8% per annum. Yale’s return compares favorably with Berkshire Hathaway’s 8.0% per annum.

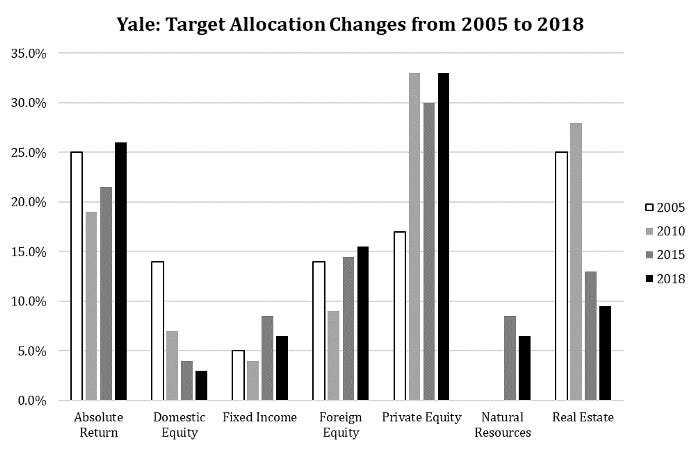

Until Yale publishes its annual report early next year, it only provides the portfolio’s “target allocation” data instead of the actual allocation data; therefore, the following analyses are based on the target allocation. In general, the gap between target and actual allocations is within +/- 2%.

As of June 2018, the largest asset class in Yale’s portfolio is Private Equity (33.0%), which includes Leveraged Buyout (15.0%) and Venture Capital (18.0%). The second and third are allocated to Absolute Return (26.0%) and Foreign Equity (15.5%). The top three asset classes represent ¾ of Yale’s overall portfolio.

In 2017, Yale’s Venture Capital allocation exceeded Leverage Buyout allocation for the first time in 20 years and even more so in 2018, partly due to its superior annualized return of 165.9% over the last 20 years.

The second largest asset class is Absolute Return (26.0%), which has increased slightly from 25.0% in 2017 to 26.0% in 2018. We had previously noted Yale’s contrary view on Absolute Return (When Other Investors Say Sayonara to Hedge Funds, Yale Increases Their Allocation, published on Oct 3, 2016), and it remains relevant even after two years.

Even before making the contrarian decision to increase its Absolute Return portfolio, Yale had started to shift its public equity exposure from the domestic markets to foreign markets. In 1985, 65% of Yale’s portfolio was allocated to the domestic equity, but today it is only 4%; whereas Yale allocates 15.5% of its assets to foreign equity.

Mr. Ted Seides, who is known for the excellent Capital Allocator Podcast, has published an article titled “When Will Yale Buy Bitcoin?” on Institutional Investor in January 2018, in which he discusses how the trend of asset allocation is formed and shaped by various institutional investors; thus in order for the cryptocurrency to become a recognized asset class, it needs more than individuals or family offices to make investments, such as endowment funds. Not exactly Bitcoin per se, but Bloomberg reported that Yale might have invested in a fund focusing on digital assets called Paradigm. This is a $400 million fund started by Fred Ehrsam, co-founder of Coinbase; Mat Huang, former Sequoia Capital partner; and Charles Noyes, ex-employee of Pantera Capital. CNBC also reported that Yale participated in Andreseen’s recent $300 million fund. It seems Yale is playing the contrarian again as many institutional investors are moving away from crypto assets due to the sharp decline in cryptocurrency prices (bitcoin is down 51% and Ethereum 70% since the beginning of the year). As a believer in the future of blockchain, Star Magnolia agrees with Yale: long on crypto assets and blockchain technology. For our views on blockchain, please read our trilogy: To Kill a Blockchain.