India’s Womenomics, A Solution to the Growth Paradox?

India’s Womenomics, A Solution to the Growth Paradox?

"…. The land of dreams and romance, of fabulous wealth and fabulous poverty, of splendour and rags, of palaces and hovels, of famine and pestilence, of genii and giants and Aladdin lamps, of tigers and elephants, the cobra and the jungle, the country of hundred nations and a hundred tongues, of a thousand religions and two million gods…” - Mark Twain

What We Knew Before Travelling to India

19 February 2024 is the day that marked my very first trip to India. My colleague, Chan Yong, and I started our week-long trip at New Delhi and we headed South to Nagpur, Mumbai, and finally Bangalore. We have heard so much about the economic rise of India in the recent years - the fast-growing GDP, the demographic dividend, and the “Make in India” ambition to surpass China to be the world’s biggest factory - yet, we have also heard so much about the other side of the coin:

(1) Yes, the GDP in India has been growing at a CAGR of 7.6% from 2013 to 2023, making it one of the fastest growing nations in the world. However, there is a critical structural issue to its GDP and that is the services sector has been long prioritized above industrial growth. India's model of growth strayed from the conventional movement of labour from farms to factories, instead focusing on the service sector. While this has created wealth much faster and generated new jobs, it has its limits in absorbing surplus labour. Currently, the services sector commands a significant portion of India's GDP, contributing about 54% while the manufacturing sector falls short, representing only about 17% of GDP (this is 30% for China). Meanwhile, employment in services (% of total employment) in India was reported at 31% in 2022.

This brings us to the second issue - (2) India has great demographic dividend, but its current set-up is not conducive to the absorption of India’s large number of surplus labour, which is estimated to reach 245 million in 2030. Employment growth has stagnated at 2% for two decades. Without reaching 4-5%, absorbing surplus labour will be impossible. The recently published India Employment Report 2024 has pegged the unemployment rate at 4.1% in 2022-23. This is equivalent to 22.7 million unemployed people.

(3) The Indian government is fully aware of the problem and hence rolled out the ambitious “Make in India” to create and encourage companies to develop, manufacture and assemble products made in India and incentivize dedicated investments into manufacturing. One of the goals of this initiative is by growing the more labour intensive manufacturing sector, India can absorb the labour surplus. However, the base of India’s manufacturing sector that constructed in a short time since its independence is still fragile and does not have good access to supply chain or the necessary infrastructure to achieve economies of agglomeration. It also further caused an employment paradox which is that there is a shortage of skilled blue-collar workers. This has resulted in stagnancy in manufacturing sector’s contribution to GDP and the government’s goal of getting that to 25% by 2025 seems unachievable.

On top of the macro concerns, corporate governance is also a prevailing issue for India. We have seen a number of scandals and shareholder disputes over the last decade. Perhaps the freshest on investors’ minds is Byju’s, a former edtech giant of India. The company was valued at $22 billion less than two years ago at the peak of its glory. Its latest valuation crashed to $250 million. Byju’s sharp decline, on the surface, was driven by missed financial report deadlines, doubts about the legitimacy of its fundraising efforts, and demands for a leadership change - but reality is that it is the result of overreliance on its founder and the failure to implement a proper corporate governance structure in the early days of the company. Another example would be Paytm, the used-to-be poster child of Indian fintech startup. The company was prohibited by the regulator from accepting deposits, credit transactions, and customer top-ups. The central bank accused Paytm of falsifying customer information and money laundering and stated that it had provided the fintech with "sufficient time" for corrective measures. The downfall of Paytm be summarized into a painful mistake of prioritizing growth above governance. It is arguable that risk of corporate governance is prevalent in all emerging markets, however, I would counter that other emerging markets have priced that risk in and hence trading at a discounted valuation, while India has not.

There are clear growth drivers, but the impediments are also difficult to ignore. Coupled with the great diversity of the country in terms of culture and language, the complexity is perhaps what has kept foreign investors (including us) away from a consistently lucrative stock market.

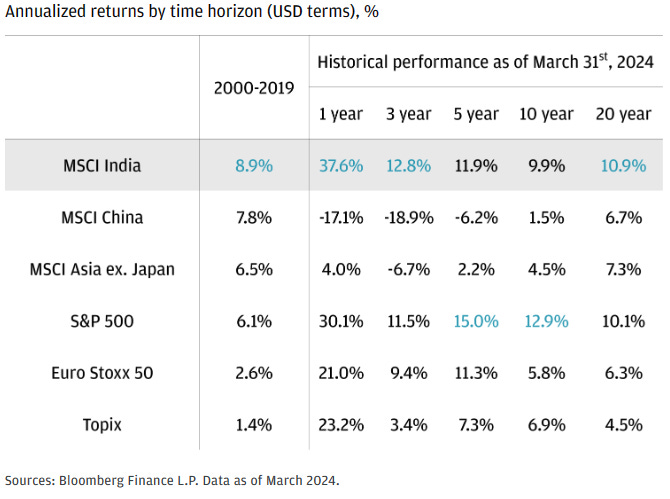

MSCI India is the only index that outperformed the S&P 500 over the last 20 years:

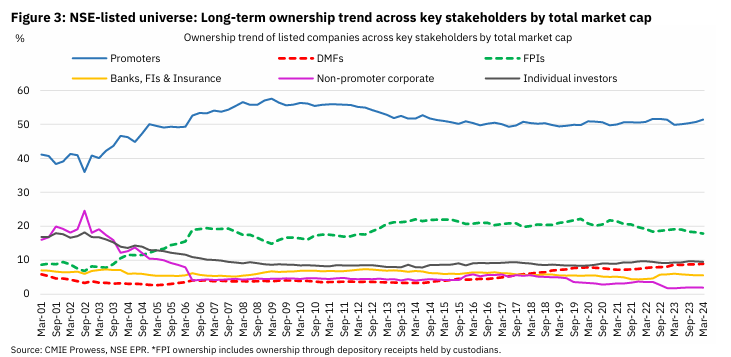

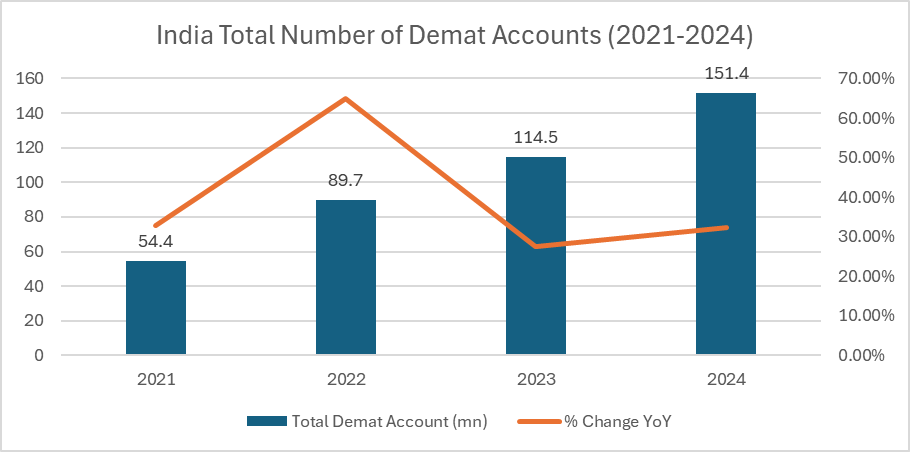

India has been the silver lining amid depressed emerging Asia, and it seems it might have more to offer. Despite all the hoo-ha in recent years, the foreign holdings (through Foreign Portfolio Investors (FPIs)) in NSE India-listed companies were only sub-18% as of March 2024 down from 19.66% in December 2018. % of ownership of FPIs in Indian listed companies has pretty much stayed in the range of 18-22% over the last 10 years. What is filling the gap and fueling India equities market is the retail investors (through Domestic Mutual Funds (DMFs)) and the Promoters. Promoters continue to be the largest owners of Indian businesses. Meanwhile, DMFs’ ownership in listed companies grew meaningfully over the last decade driven by the growth in retail demat accounts (short for 'Dematerialization,' it is a digital vault for stock investments in India). The total number of demat accounts surged to a record high of 151.4 million by the end of March 2024. This is expected to continue to grow rapidly given only 7% of Indian household financial assets is in equities and mutual funds, compared to 50% in US and 41% in China. What this means is that more than ever before, the impact on Indian bourses is now linked to what the local investors do, indicating that local insights will be increasingly important.

Source: Star Magnolia Research, Business Standard India, data as of March 2024

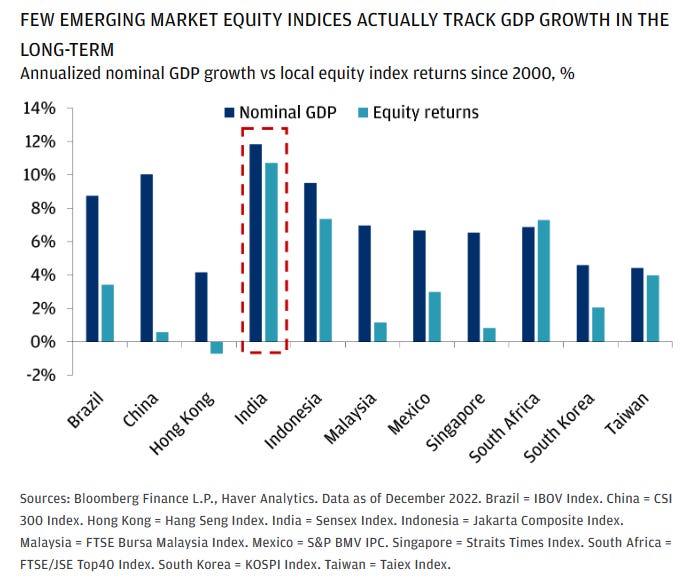

Another interesting aspect of the India stock market is its correlation to fundamentals. Intuitively, higher GDP growth should translate to higher company earnings, which should result in higher equity returns. However, this is often not the case for emerging markets. From the chart below put together by JP Morgan, it is apparent that India is one of the rare few markets that generated stock market performance that is highly correlated to its GDP growth. As believers of fundamental investing, we want to be in a market that its rise is driven by rising corporate profits and India seems to be able to offer that.

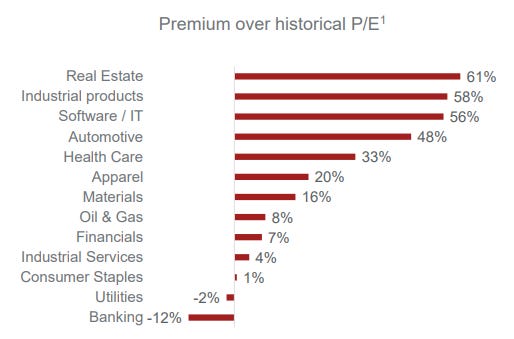

At the same time, valuation has always been difficult to digest in India with euphoria observed in various sectors, such as real estate, industrial products, and software which are seeing over 50% premium over historical P/E ratio. India has always commanded rich valuation and from what we could see, value investors tend to do less well in India. However, that does not mean we want to join the hype, instead, our goal is to find the best of both world with high quality asset managers that can identify great companies with sustainable growth at reasonable valuation.

*Based on 750+ companies listed in India, excluding outliers (<5x P.E and >100x P/E), comparison of P/E as on 26 Sep 2023 with average P/E over Sep’09 to Sep’19 (to avoid COVID noise)

Source: Arisaig Partners, Bloomberg

With these in mind, we hopped on our flight to see India with our own eyes and in search for the right Indian asset manager.

Observations On the Ground

“It's important to teach our female youth that it's OK to say, 'Yes, I am good at this,' and you don't hold back.”” - Simone Biles

Source: Star Magnolia Research, photo taken during household visit in Nagpur

Consumer Upgrade Surely, But More Importantly…

During our time in India, we were very fortunate to be given the opportunity to visit several lower-middle ($300-$1,200/month) to middle class households ($1,200-$3,000) and interview the homemakers. There are a projected 600 million consumers in India to enter middle class in the next 25 years and we were hoping to gather some insights on their aspirations. The key insights we have gathered are as followed:

(1) More Women in the Workforce = Change in Consumption Pattern

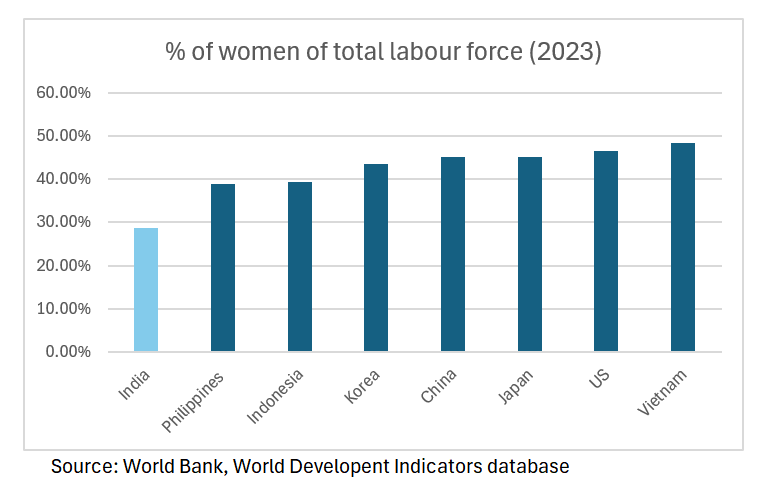

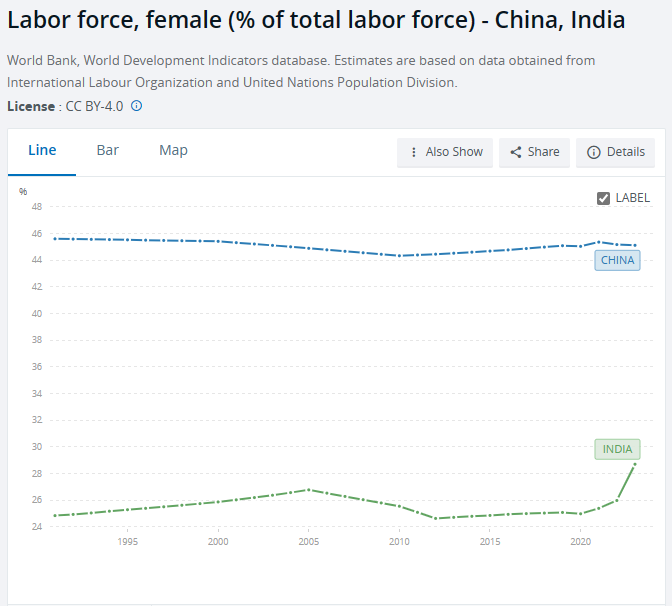

One consistent voice we heard from the mothers is that all of them want their daughters to be educated, to have a career, and to get married only after they achieved the first two. We find this incredibly encouraging as India has been significantly lagging behind not just developed countries but also other developing countries in percentage of women in labour force because of social stigma.

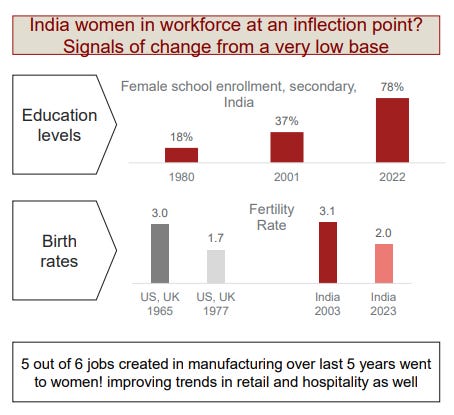

It is only in the recent years (post-2020) that we began to see a huge uptick in women joining the labour force. We believe more is to come as more Indian women are getting educated, fertility rate is coming down, more non-farm jobs became available, and social stigma is changing (as we can see from our interviews with the households).

Source: Arisaig Partners

The “Hockey Stick” moment for Indian women:

Source: Statista

Much research has shown the advantages of a gender diverse workforce - higher profitability, better productivity, and there are simply too many talented women to be left behind when they can do so much more for the world. A 2018 McKinsey report estimated that India could add $550bn, or 16%, to its GDP by increasing its female labour force participation by just 10%.

In response to our concerns over the employment paradox, we were happy to learn that women are landing jobs in manufacturing sector and the rise of travel industry (think air stewardess)/care economy is also creating new job opportunities for women. This is because employers prefer to hire women to men when it comes to certain roles as women are regarded as more patient, cooperative, and attentive to details than their male counterparts. By taking better advantage of the skills and talents of half its population (the women), India may potentially fix its employment paradox.

And the benefit does not just stop there. Women are also the largest consumers. Globally, women drive 70-80% of all consumer purchasing through buying power and influence. Just imagine what would happen to their consumption pattern once they become salary makers. From our interviews with Indian households, it’s not difficult to predict huge growth in beauty and personal care/fashion wear in the next decades.

(2) The Next Generation is Different

During one of our household visits in Nagpur, an eleven-year-old girl told us, “India does not need the caste system, India needs more opportunities.” The same girl idolizes Korean popstars and wants to move to Korea permanently. Another girl in her teens from another Nagpur household giggled when we asked her how many shoes she has compared to her mother and the answer was more than double of her mother’s. She also got most of her apparel online or from retailers such as Zudio unlike her mother who goes to the markets. In another household at Delhi, the mother was telling us she had to learn how to make pizza because her kids insisted on having one.

These anecdotes all point to one thing - the next generation of India is a different species of consumers. They are more digital savvy, bigger spenders with a more global taste, and more individualistic.

And this trend is further propelled by the following -

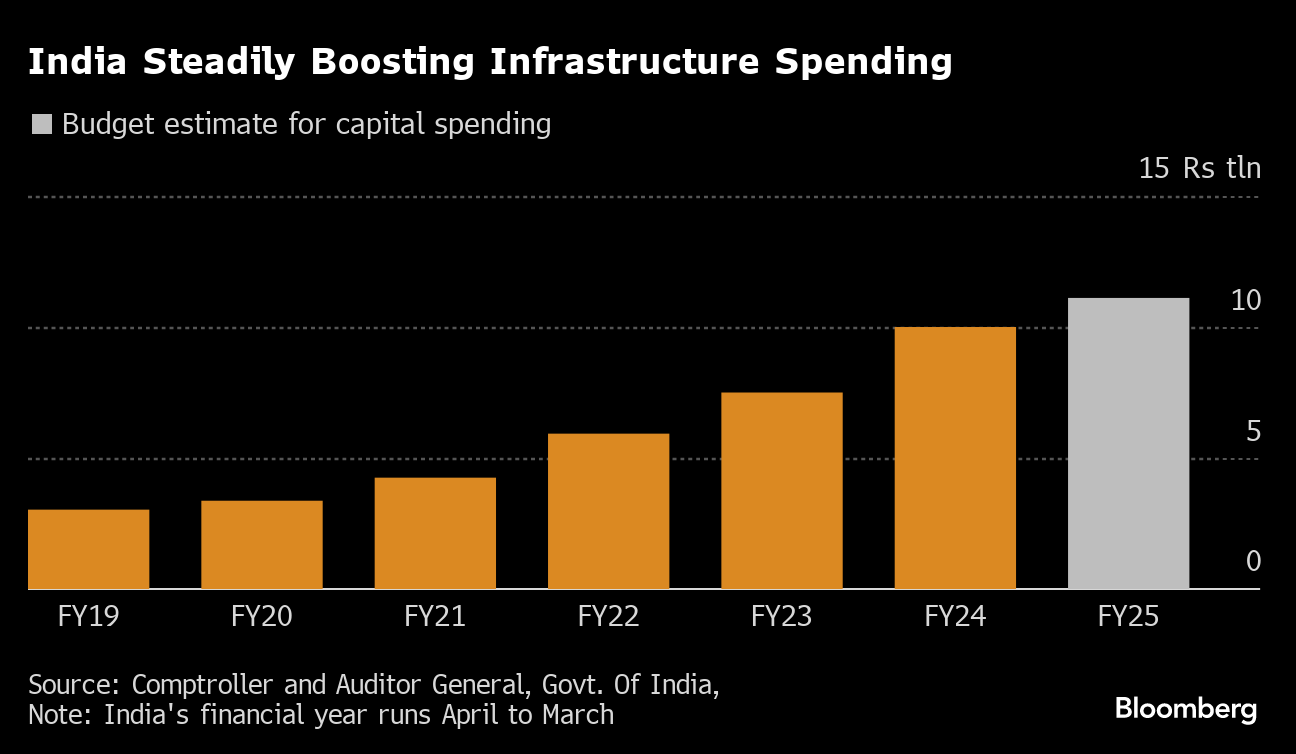

(3) The Infrastructure Spending is Beginning to Payoff

Chan and I took the metro at Nagpur (tier 2 city), and it was amazing. It was clean, fast, and steady. And it is just one of the outcomes of the many infrastructure projects undergoing in India.

Source: JP Morgan

The government has spent a whopping $276 billion on infrastructure spending over the last three years (FY22-FY24). The infrastructure focus is apparent when one looks at the capital spending to GDP ratio which has almost doubled from 1.6% of GDP in 2018-19 to 3.2% of GDP in 2023-24. Of this, the major push has come in building roads, highways, and railways. Furthermore, the government has incentivised states to jump on the infrastructure bandwagon by offering long-term interest free capex loans in recent years.

Though India is often slow in execution, the investment has begun to pay off - India’s ranking in the World Bank’s Logistics Performance Index (LPI) jumped up 6 places to 38 in 2023 from 44 in 2018 with significant improvements in infrastructure surrounding international shipments and India’s logistics quality.

Infrastructure is, obviously, crucial to the economy development of a country. It can strengthen the weak foundation of India’s manufacturing sector. It can greatly improve efficiency, enhance connectivity, create jobs, attract investments, and improve quality of life for the people. Better infrastructure means it is safer for women to go to work. We can also almost see Indian youth jumping on a metro to a mall that was previously difficult to access to eat pizza and shop at Zudio (think India’s Zara) and Nykka (think India’s Sephora).

It is not difficult to tell that we enjoyed our trip to India and became a lot more optimistic about investing in the country. The big question remaining is governance.

The Question Around Governance

Based on our conversations with Indian asset managers, those that we believe are high-quality have shared similar sentiments on corporate governance:

(1) Filtering out the bad apples is half of the job; (2) stewardship and active engagement can make a difference. Indian asset managers were generally realistic with respect to current stewardship activities, recognizing both the progress made over the past decade but also that India is often “two step forward, one step back”. The ability to identify and filter out bad actors is critical for long-term success as an investor in India, and this is best done with on-the-ground, local knowledge and expertise. The upside can then be created with stewardship and engagement as sometimes, it’s not that the companies want to do “bad”, but because they do not know the standard of “good”. By helping Indian companies understand best practices, investors will be able to generate sustainable long-term return. We were very encouraged by this shared sentiment across asset managers in both public and private markets. Even for venture investors, who tend to focus less on governance given the early stage of the company, have expressed the importance of building the right governance structure as early on as possible in the company’s life.

In conclusion, the story of India is a tale of two cities - India's economy continues to face structural challenges such as its employment paradox, a foundationally fragile manufacturing sector, and prevalent corporate governance issues. Despite these concerns, there are clear growth drivers including a rising middle class, increased female workforce participation, and significant infrastructure investments that are paying off. From our on-the-ground visits, we saw a positive shift in consumer behavior, particularly among younger generations and driven by women going into workforce, and a potential for improved governance through active engagement by asset managers. We believe that India’s stock market performance will continue to be closely correlated to the fundamentals of the businesses, and it is important to partner with high-quality Indian managers to participate in the next decade of India’s growth.